Many people use trusts. For holding investments, running a business and a number of other reasons. They’re simpler, more flexible and less regulated than companies. They offer asset protection, wealth succession outside of deceased-estate regulation, and greater anonymity, and they’re usually more tax effective. Over the year, our team at Nexia Australia have been waiting for these high anticipated pronouncements from the ATO.

Anti-avoidance shadow over trusts

Since it was enacted in the 1970s, section 100A of the Income Tax Assessment Act 1936 has cast a shadow over trusts, but hasn’t spooked the taxpayer community as much as it perhaps should have. The likely reason is that many regard section 100A as a bit “disco”, in that it targeted promoted tax schemes from the 1970s using trusts, which were the purview of only a relatively small number of wealthy people.

However, with almost all of us nowadays having trusts in our tax affairs, we are all capable of offending section 100A. It’s just that, because section 100A is aimed squarely at schemes of its era, it forces a 1970s square peg into a present-day round hole. Also, until recently, case decisions on these anti-avoidance rules tended to involve promoted schemes from the 1970s that wouldn’t work today because of other anti-avoidance rules enacted since. There are two section 100A cases presently before the courts that were not promoted schemes, but each reflect very different circumstances. In one, section 100A was found not to apply, and in the other, it was held that section 100A did apply. Both decisions are on appeal.

Trust behaviour targeted

There are a number of components to section 100A, and a wide berth of interpretation for what might or might not be caught in its web. The crux of it is appointing trust income to a beneficiary under what is called a “reimbursement agreement”. Don’t be fooled by the label – no “reimbursing” of any kind is required. The kinds of scenarios possibly – but not necessarily – offending the provision can be succinctly summarises as follows:

You appoint trust income on paper to a beneficiary on a lower tax rate, but someone else gets the benefit of the underlying funds, and there is a purpose of achieving a tax saving.

Imagine the common scenario of appointing trust income to your adult child, on which income tax of up to 21 cents (including Medicare levy) is borne. That of itself may well be fine, but further imagine that you took the underlying money. That means you have 79-plus cents in the dollar in your hands. But if you had instead appointed the income to yourself and paid, say, the top income tax rate of 47 cents, you would have had only 53 cents in your hands. You can see the tax mischief possibly in play.

The above scenario wouldn’t necessarily amount to a reimbursement agreement that offends section 100A – there’s a fair bit more to it. That includes having to consider an exclusion from section 100A of an agreement “entered into in the course of ordinary family or commercial dealing”. Note that that looks to the process you went through, not the actual outcomes. Particular questions would need to be asked about the broader circumstances, processes and intentions. Everybody’s story would be different, and it is these differences in the details that would determine whether section 100A has been offended.

Where an appointment of trust income is found to have arisen from a reimbursement agreement, section 100A has the effect of the trustee being assessed at 47%, and penalties may apply. There is no limitation on how far back the ATO can go to apply section 100A.

ATO’s views

Earlier this year, the ATO released a draft ruling setting out their views on numerous components of section 100A, what circumstances do or don’t offend the provision. They also released a draft Practical Compliance Guideline (PCG), which provides guidance on whose trust arrangements the ATO will investigate further, and whose they’ll leave alone. These pronouncements generated quite a ruckus. But it seems the ATO has listened to feedback, with the final versions released yesterday featuring a number of changes. We are pleased to see that several sensible changes Nexia proposed in our submission have been incorporated into the final versions: Taxation Ruling TR 2022/4 and PCG 2022/2.

Will the ATO review your tax affairs?

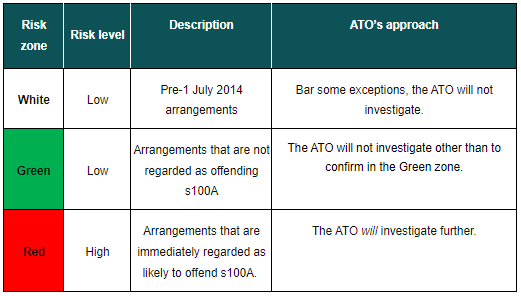

The PCG sets out a zone system for the application of compliance resources. Which zone your trust arrangements for any particular year fall into will determine the likelihood of the ATO investigating further. The PCG sets out a number of examples and guidance for when arrangements fall into the following zones:

The above has been simplified from the draft by eliminating an entire zone (Blue), which captured scenarios that, on the surface, could not be categorised as low or high risk, and required further investigation. The number of examples of Green-zone scenarios has been expanded, which, pleasingly, will capture a number of common situations that would have fallen into the draft version’s Blue-zone void.

Ordinary family or commercial dealing

What exactly is or is not within this exclusion from section 100A has been hotly debated. This was intended to distinguish the ordinary operation of trusts – at the time, used by few people – from promoted schemes of the time. But, as noted above, the very different circumstances of today, with the widespread use of trusts, are having to contend with anti-avoidance laws that haven’t changed in 40 years.

Next steps

We will be immersing ourselves in these final pronouncements and provide more specific, considered comment next week. We will also provide further guidance in the coming months and beyond.

As to whether your specific circumstances are impacted, there are two branches to consider:

- Looking back: Consideration ought to be given as to whether the ATO might regard the circumstances of any past appointments of trust income as offending section 100A, given the finalised views expressed. And if there is an appreciable risk of that being the case, what actions might redress that.

- Looking ahead: Past practices and decisions as to the appointment of trust income might require reassessment as to whether they continue to be appropriate.

Talk to your trusted Nexia Edwards Marshall NT adviser – we’ll certainly be talking to you in due course – about managing your trust income appointment decisions in light of these final pronouncements from the ATO.