The Australian Charities and Not-for-profits Commission (ACNC) was established in 2012 as the national regulator of charities in Australia. At that time, the ACNC Act introduced financial reporting requirements for charities which varied depending on the size of the charity, where size was based on the charity’s total annual revenue for the relevant reporting period.

The ACNC Act required that a review be undertaken after its first five years of operation to assess whether, among other things, the Act was fit for purpose and if any amendments were required. A review in 2018 found that current revenue thresholds for determining the different financial reporting requirements were too low. The review found that increasing the thresholds, so fewer charities are required to provide annual financial reports, would reduce the compliance burden of registered entities.

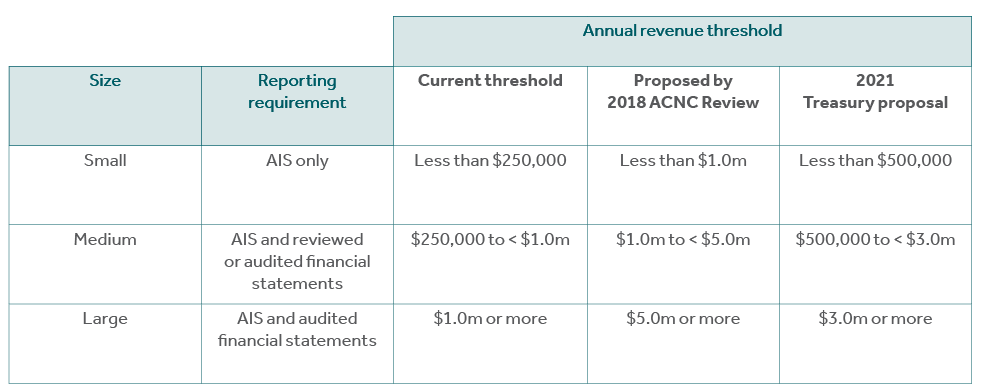

As a result, Treasury has issued proposals to increase the size thresholds for small, medium and large charities, with consequential effects on their financial reporting obligations. A comparison of the current size thresholds; those recommended by the 2018 review; and Treasury’s proposals are:

Charities that move from medium to small are not required to submit reviewed or audited financial reports to the ACNC but they will still be required to submit an Annual Information Statement, which includes information about the charity, its governance and activities and basic financial information (revenue, expenses, assets and liabilities).

Charities can be established using various structures which can result in different regulatory and reporting regimes. For example, if an ACNC registered charity is an incorporated association, as well as its ACNC reporting requirements, it will also have a separate reporting requirement to the State where it is incorporated, and possibly different thresholds at which these requirements apply. While ACNC-registered charities that are incorporated associations in South Australia, Tasmania and the Australian Capital Territory would immediately benefit from an increases in ACNC reporting thresholds, other States and Territories have different reporting thresholds for incorporated associations. The Council on Federal Financial Relations has asked that Commonwealth and State officials develop a framework to harmonise financial reporting thresholds for incorporated associations across jurisdictions by 30 June 2021.

Nevertheless, increasing the ACNC reporting thresholds may not directly assist all entities that undertake fundraising activities. All States, except New South Wales and Queensland, currently accept the financial report a charity lodges with the ACNC as meeting their fundraising reporting requirements. Queensland currently requires all entities conducting fundraising, regardless of size, to submit audited financial statements. The New South Wales Government appears to be committed to maintaining reporting thresholds for authorised fundraisers, currently set at $250,000.

While these changes will effect which entities will need to prepare annual financial statements, it does not affect what form those financial statements will take. Treasury’s proposals only addresses the reporting thresholds and does not deal with whether the ACNC will continue to accept special purpose financial reports. That will depend on the outcome of the AASB’s project on a new not-for-profits reporting framework, which is exploring which not-for-profit entities will be required to prepare general purpose financial statements and their basis of preparation – Tier 1 full GPFR; Tier 2 SDS; and a possible new Tier 3. But that’s a topic for another day.

In case you missed it

From 18 February 2021 new laws affect when a director’s resignation takes effect and prohibits resignations that leave a company with no remaining directors.

Previously, a director could resign simply by giving notice to the company. The company was then required to notify ASIC of the director’s resignation within 28 days or pay a late fee. Under the new law, where ASIC is not notified of a resignation within 28 days, the effective date of the resignation will be when ASIC is actually notified.

For example, a director resigns on 1 April 2021 and neither the company nor the director notifies ASIC of the resignation until 15 December 2021. ASIC will record the director’s resignation date as 15 December 2021, as notification occurred more than 28 days after the purported date the person ceased being a director. As a consequence, for the purpose of the Corporations Act 2001 the person is taken to still be a director during that intervening period, with all the obligations and duties that entails.

The Act also prohibits companies from removing the last remaining director identified on ASIC records, thereby leaving a company with no directors.

To find out more on how this change affects directors and charities registered with the ACNC, and what directors can do to limit their exposure, read the full article on Nexia Australia’s website here.