The Federal Budget for 2019-20 contains a number of tax and superannuation announcements affecting small and middle-market business owners, including:

- Reductions in personal income tax and increases in personal rebates.

- Wider eligibility for the instant asset deduction, extended time, and increase in threshold to $30,000.

- Additional funding for the Export Market Development Grant scheme.

- Risk losing your ABN if tax returns are outstanding.

- Minor improvements in superannuation flexibility.

An election is expected to be called this weekend for mid-May. That means there is uncertainty about whether these measures will be enacted especially if a change in government occurs.

In the meantime, we set out a summary of the key measures announced, and what they will mean for you.

To discuss the budget in more detail and how it may impact your personal or business situation, contact Sarah McEachern or your Nexia Edwards Marshall NT Adviser to get your tax affairs in order by 30 June.

Individuals

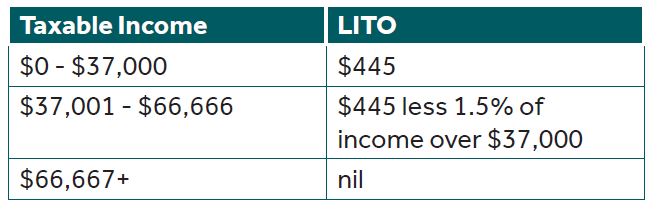

1. Low-Income-Tax-Offset

Background

The low-income-tax-offset (LITO) is a non-refundable rebate that reduces the tax payable by individuals whose incomes fall below $66,667 in an income year.

The LITO rates currently in force up to and including the 2021-22 income year, are:

In the 2018 Budget, the Government announced that from 2022-23 the maximum LITO would increase to $645. This will coincide with the removal of the low-and-middle-income-tax-offset (LMITO) from that same year.

Announcement

While the LITO rate for 2018-2019 to 2021-2022 remains unchanged, the Government has announced that the maximum amount of the rebate available to taxpayers from 2022-23 will increase from $645 to $700.

What this means for you

From the year ending 30 June 2023, the change in LITO rates will take effect as follows:

* The upper threshold was originally set to $41,000

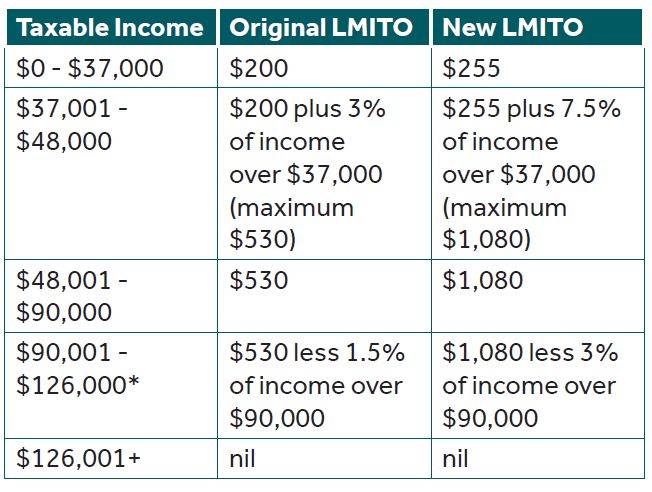

2. Low-to-Middle-Income-Tax-Offset

Background

The low-and-middle-income-tax-offset (LMITO) is a non-refundable rebate that reduces the tax payable by low- to middle-income earners. The LMITO was originally announced in the 2018 Budget to apply from the 2018-19 income year up to and including the 2021-22 income year.

In addition to the LMITO, low-income earners may also be entitled to the existing low-income-tax-offset (LITO).

From 2022-23 the existing LITO and LMITO regimes will be replaced by a single LITO regime (see ‘Low-Income-Tax-Offset’).

Announcement

The 2019 Budget increases the amount of the rebate available to taxpayers.

The maximum rebate available will increase from $530 to $1,080 per annum, while the base amount will increase from $200 to $255 per annum.

What this means for you

The rebate will become available to taxpayers upon lodgement of their individual tax returns.

For the year ending 30 June 2019 a taxpayer will be entitled to the rebate upon lodging his or her 2019 tax return.

The amount of the rebate to which a taxpayer is entitled is based on the taxpayer’s income for the year. The difference between the LMITO amount announced in the 2018 Budget and the LMITO amount announced in the 2019 Budget is shown below:

A taxpayer on an income of, say, $50,000 for the 2018-19 year will be entitled to a $1,080 LMITO and a partial LITO per Item 1 above.

* The phase-out threshold was originally set at $125,333

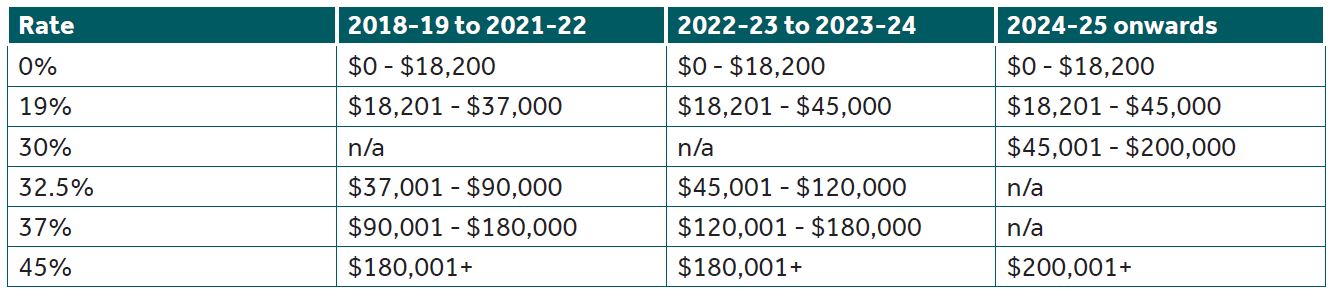

3. Marginal Tax Rates

Background

Currently, personal income tax rates for Australian residents are:

Note that these rates do not include the 2% Medicare levy.

Announcement

To coincide with the removal of the low-to-middle-income-tax-offset in 2022-23 noted above, the Government has announced that the top threshold for the 19% tax rate will increase from $41,000 to $45,000.

The 32.5% marginal tax rate will reduce to 30% from 2024-25.

What this means for you

The new rates will apply as follows:

From 2024-2025, about 94% of taxpayers will have a marginal tax rate of 30% (plus 2% Medicare levy) or less.

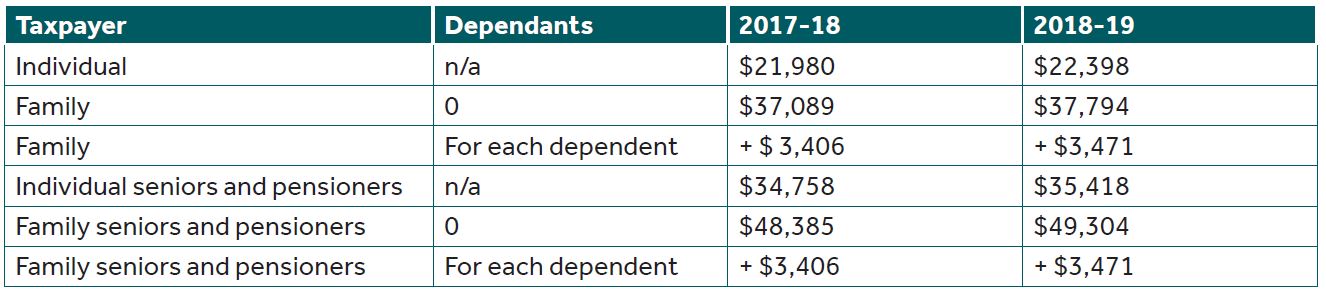

4. Medicare Levy

Background

The Medicare levy is imposed at a rate of 2% based on a set of income thresholds below which the taxpayer has no liability. Liability for the Medicare levy applies in addition to personal marginal income tax rates.

Announcement

The income thresholds for all taxpayers will increase from the 2018-19 income year to take account of recent CPI movements.

What this means for you

The new income thresholds for 2018-19 below which no Medicare levy is imposed, are as follows:

5. Proposed removal of the capital gains tax (‘CGT’) exemption for the family home when you become a foreign resident

Background

In the 2017-18 Federal Budget, the Government announced that your family home would lose its tax-exempt status upon your becoming a foreign resident.

This was widely viewed as being harsh, as it would retrospectively deny the CGT exemption.

Announcement

No announcement on the proposed changes has been made in the 2019-20 Federal Budget.

What this means for you

The Bill giving effect to the proposed changes is yet to be passed by Parliament. There are only two sitting days for Parliament before the Federal election will be called. The Bill is not listed for consideration on either of these days.

Therefore the Bill will lapse upon Parliament being dissolved. We are unaware whether a re-elected or newly-elected government will resurrect this measure after the election.

Businesses

1. Instant asset write-off increased to $30,000, wider and extended access

Background

Currently, businesses with group-wide turnover below $10 million can fully deduct the cost of most depreciable assets that cost less than $20,000. The cost of depreciable assets costing $20,000 or more is deducted over several years. The cost threshold for the instant deduction was due to return to the standard $1,000 on 1 July 2019.

Announcement

For depreciable assets acquired after 2 April 2019, the threshold will increase to $30,000, and the write-off will be available for a further 12 months to 30 June 2020. Further, the turnover limit will be increased to $50 million.

What this means for you

Any urgency to acquire assets by this coming 30 June is abated. You can wait until after, and the instant deduction at the higher threshold will still be available until 30 June 2020. Also, the higher turnover limit of $50 million turnover will significantly increase the number of businesses eligible for the write-off.

We note that the best reason to acquire any new asset is not a tax write-off, but rather the judgement that your business will earn a sufficient commercial return from investing in that asset. The full tax deduction is merely a timing difference – you would normally deduct the cost over several years anyway – and should be viewed more as a bonus to the commercial return.

2. Amendments to Division 7A private company loan rules

Background

Companies pay tax at 27.5% or 30%, whereas their shareholders may pay tax at higher personal rates. Division 7A is an anti-tax avoidance regime to prevent shareholders from accessing company profits in a tax-preferred manner – usually by way of a loan – without paying the difference of tax between the company tax rate and the shareholders’ personal tax rate. Breaching Division 7A usually triggers a deemed assessable dividend to the shareholder or related party.

A number of long-awaited amendments to Division 7A were proposed to start on 1 July 2019, as well as possible other amendments arising from a Treasury Consultation Paper released in October 2018. Proposed changes included:

- Simplified loan repayment terms;

- Self-correction mechanism to rectify breaches;

- Legislating to bring trust unpaid present entitlements (UPE) into Division 7A;

- Replacing both the 7-year and 25-year loan terms with a standard 10-year maximum term;

- Abolishing the distributable surplus limit on the amount of a deemed dividend; and

- Bringing grandfathered pre-1997 loans into Division 7A.

Announcement

The start date for any changes to Division 7A will be deferred a further 12 months to 1 July 2020. Nexia Edwards Marshall made this recommendation in our submission response to Treasury’s 2018 Consultation Paper, and we are encouraged that our submission was heeded.

The Government and Treasury will use this additional to time to consult with the community to refine the proposed amendments.

What this means for you

Whilst uncertainty remains about how Division 7A will be amended, the upside is that more time will be available to advocate further on behalf of our business clients for sensible reforms to this regime.

3. Increased funding for the Export Market Development Grant scheme

Background

The Export Market Development Grant (‘EMDG’) scheme is a Federal Government financial assistance program that aims to support businesses to develop export markets through marketing and promotional activities.

Announcement

The Government will invest a further $60 million in the EMDG scheme over the next three years. By way of comparison, the EMDG scheme made grants totalling $131.6 million to qualifying exporters in the 2017-18 year.

The increased funding is intended to help businesses obtain more exposure in international markets and generate additional exports for Australia.

What this means for you

The scheme reimburses applicants up to 50% of eligible export promotion expenses – subject to certain conditions and limits. If you are developing overseas markets, or looking at expanding internationally, you may be eligible for a grant under this scheme. Nexia Edwards Marshall can assist you in reviewing your eligibility and submitting your application.

4. Increased refunds of Luxury Car Tax for primary producers and tourism operators

Background

Currently, eligible primary producers and tourism operators may be eligible for a partial refund of the Luxury Car Tax paid on eligible four-wheel or all-wheel drive cars, up to a maximum of $3,000.

Announcement

For vehicles acquired on or after 1 July 2019, eligible primary producers and tourism operators will be able to apply for a refund of any Luxury Car Tax paid, up to a maximum of $10,000.

What this means for you

Eligible primary producers and tourism operators should take the increased concession into account in planning future purchases of vehicles subject to Luxury Car Tax. The eligibility criteria for primary producers and tourism operators and the types of vehicles eligible for the concession will remain unchanged.

5. Black Economy – strengthening the Australian Business Number system

Background

Currently, ABN holders are able to retain their ABN even where they are not complying with income tax return lodgement obligations and/or the obligation to update their ABN details.

Announcement

As part of the conditions for holding an ABN, ABN holders with an income tax return obligation will be required, from 1 July 2021, to lodge their income tax return and, from 1 July 2022, to confirm the accuracy of their details on the Australian Business Register annually.

This measure is expected to disrupt black economy behaviour.

What this means for you

ABN holders risk losing their ABN if income tax returns remain outstanding or if they do not confirm annually the accuracy of details on the ABN register. Without an ABN, your business customers are required by law to withhold 47% of any payment to you.

6. Queensland Disasters – Grants for recovery, tax exemption

Background

The Fassifern Valley (90 kms to the southwest of Brisbane) suffered severe damage to crops and farm infrastructure in a severe hail storm in October 2018. The Federal Government has provided a grant to those affected through the Foundation for Rural and Regional Renewal.

A monsoonal trough dumped rain across the Northern Queensland region from 25 January 2019 through to February 2019 causing widespread flooding and huge losses of stock and farm infrastructure. Affected primary producers, small businesses, and non-profit organisations are eligible for Category C and Category D grants under the Disaster Recovery Funding Arrangements 2018, On-Farm Restocking and Replanting grants, and On-Farm Infrastructure grants.

Announcement

These grants will be exempt from income tax and will be classified as non-assessable non-exempt income.

What this means for you

Recipients of these grants will not pay income tax on these grants, nor will they reduce any carried-forward tax losses.

7. Tax avoidance taskforce funding boost

Announcement

The Government will provide $1 billion to extend the ATO taskforce’s compliance activities targeting multinationals, large public and private groups, trusts and high-wealth individuals.

Additional funding will also be provided to the ATO and Treasury to increase their capabilities to analyse taxpayer data.

What this means for you

The authorities’ increased ability to interrogate and cross-match vast quantities of data to uncover anomalies increases the risk of a review or audit by the ATO. More than ever, the integrity and consistency of your information provided in the myriad of disclosure forums with the ATO is paramount.

Superannuation

1. Improving superannuation flexibility for older Australians

Background

Currently, people aged 65 to 74 can only make voluntary superannuation contributions if they self-report as working a minimum of 40 hours over a 30-day period in the relevant financial year. People aged 65 and over cannot access bring-forward arrangements. People aged 70 and over cannot receive spouse contributions.

Announcement

From 1 July 2020, the Government will allow both concessional and non-concessional voluntary contributions to be made by people aged 65 and 66 who do not meet the work test. People aged 65 and 66 will also be able to make up to three years of non-concessional contributions under the bring-forward rule. People aged 74 or younger will be able to receive spouse contributions, with people aged 65 and 66 no longer needing to meet the work test.

What this means for you

These new measures align the work test with the eligibility age for the Age Pension, and increase the age limit for spouse contributions to give older Australians greater flexibility in planning for retirement.

2. Superannuation Funds – Simpler Reporting of Exempt Income

Background

Superannuation Funds that have members in both pension and accumulation phases must calculate the amount of the fund’s income that is income tax exempt (attributable to pension phase income) or taxable (attributable to accumulation phase income). This has become particularly important for members with balances in excess of $1.6 million. In such cases an actuarial certificate has been required under the law to ascertain the exempt income.

Announcement

Superannuation funds that use the proportionate method where all members are in pension phase for the whole of the income year will no longer be required to obtain an actuarial certificate.

What this means for you

While exact calculations will still need to be undertaken to determine exempt pension income, actuarial certificates will no longer be required, provided the above conditions are met.

This measure commences on 1 July 2020.

3. Insurance for Members of Superannuation Funds with Low Balances

Background

Superannuation funds have been required to offer insurance for members. Last month, a law was passed to ensure that superannuation fund trustees stop providing insurance on an opt-out basis from 1 July 2019 to a member whose member account has been inactive for longer than 16 months unless the member requests the insurance to continue.

Announcement

In contrast, insurance will be offered only on an opt-in basis where member balances are less than $6,000 and where the new member is less than 25 years of age.

What this means for you

This measure allows young people with low superannuation balances to opt-in to have their superannuation funds deduct insurance premiums from their member balances. Many will choose not to opt-in thereby preserving their superannuation balances.

The start date for this measure has been extended from 1 July 2019 to 1 October 2019.

4. Increased budget for ATO compliance activities

Announcement

The Government will provide an additional $42.1 million to the ATO over four years to increase compliance activity directed at recovering unpaid tax and superannuation liabilities.

What this means for you

The focus of these activities is ensuring on-time payment of tax and superannuation liabilities by larger businesses and high wealth individuals, which is another good reason to ensure all tax compliance obligations are met. This measure is not directed at small business.

International

1. Australia-Israel tax treaty

Background

On 28 March 2019, the Government signed a tax treaty with Israel and will introduce amendments to give the treaty the force of law in Australia as well to provide that certain income covered by the tax treaty is deemed to have an Australian source.

Announcement

When incorporated into Australia law, the Australia-Israel tax treaty will relieve double taxation, lower interest, dividend and royalty withholding tax and improve certainty for taxpayers in both Australia and Israel.

What this means for you

Australians with connections to Israel and Israelis with connections to Australia should carefully consider the Australia-Israel tax treaty to determine its impact on them.

Your Nexia Edwards Marshall Adviser will be pleased to advise you on all aspects of this and any other tax treaty to which Australia is a party.

2. Updating the list of information exchange countries

Background

The tax legislation lists countries that have entered into an effective information sharing agreement with Australia in order to combat offshore tax avoidance and evasion. Residents of listed countries are able to access a reduced withholding tax rate of 15%, instead of the default rate of 30%, on certain distributions from Australian Managed Investment Trusts.

Announcement

The list of information exchange countries will be updated to include Curaçao, Lebanon, Nauru, Pakistan, Panama, Peru, Qatar and the United Arab Emirates, effective from 1 January 2020

What this means for you

From 1 January 2020, residents of the abovenamed countries should be able to access a reduced withholding tax rate of 15%, instead of the default rate of 30%, on certain distributions from Australian Managed Investment Trusts, because the governments of those countries have established a legal relationship allowing them to share taxpayer information with Australia.

Other

1. Extending Deductible Gift Recipient (‘DGR’) status to Men’s Sheds and Women’s Sheds

Background

Taxpayers are entitled to a tax deduction for donations made to a DGR. An entity must be specifically listed as a DGR in the Tax Act to be a DGR, or must belong to a general category of DGR listed in the Tax Act.

Announcement

The Tax Act will be amended to include a new general category of DGR for Men’s Sheds and Women’s Sheds from 1 July 2020.

What this means for you

Men’s Sheds and Women’s Sheds provide a safe, friendly and welcoming environment where men and women are able to work on meaningful projects at their own pace in their own time in the company of other men or women respectively. To encourage this philanthropic cause, you will be able claim a tax deduction for donations made to this new category of DGR from 1 July 2020.