The existing JobKeeper program comes to an end on 27 September. The next phase of the program runs from 28 September to 28 March 2021. We had previously outlined the next phase, based on announcements made.

Yesterday, the legislative Rules for this next phase were registered, and this has now given us details on a few things that were lacking clarity. If you are already enrolled in the program, there is no need to re-enrol for the next phase. If you qualify for the next phase, all your eligible employees (1 March-based and 1 July-based) will simply carry over.

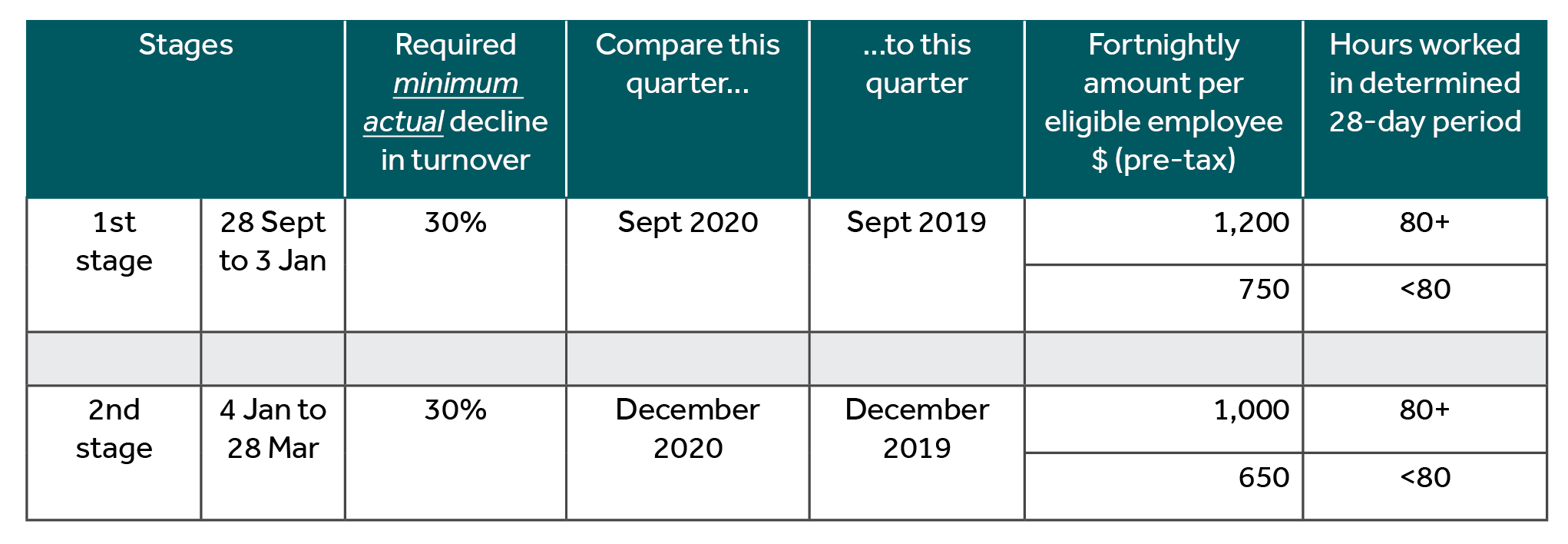

To recap, here is a summary of the next JobKeeper phase (assuming the 30% decline threshold applies):

From 28 September, JobKeeper will be tapered, making it more targeted. If you are not in the existing JobKeeper program, you can still qualify for the next phase. You’ll need to satisfy the same qualifying criteria, and the new actual decline in turnover test. You can qualify for either the 1st stage or the 2nd stage. The first monthly declaration for the next JobKeeper phase will be for October, incorporating the first two fortnights, ending 11 October and 25 October. We expect the declaration will be similar to before, except that each eligible employee will be allocated to the higher-rate or lower-rate camp.

Here are some of those finer points that are now clearer, including what you need to do.

Decline in turnover – re-test

The re-test is based on decline in actual turnover. For stage 1, compare the September 2020 quarter to the September 2019 quarter. For the stage 2, compare the December 2020 quarter to the December 2019 quarter. For businesses, the required decline is either 50% or 30%, depending on the group-wide turnover (above/below $1 billion). However, when the original JobKeeper commenced, determining the relevant percentage was based on group-wide turnover in the 2019/20 and 2018/19 income years. But now we’ve crossed into a new income year. Accordingly, for the purposes of the new JobKeeper phase, measuring group-wide turnover will be based on the 2020/21 and 2019/20 income years. This means that, where the level of turnover has changed, it is possible that you could now be subject to a different decline percentage.

Whatever the applicable decline percentage, it is still the case that only the turnover of the particular entity is used for actually measuring any decline.

To avoid a re-run of the saga over differing methods of measuring turnover, the Commissioner of Taxation has been given the power to determine that turnover essentially means what you disclose in your Business Activity Statements (BAS), and he is expected to so determine. The Commissioner already had the power to determine alternative decline in turnover tests where there is no comparative period in 2019 (eg, recently commenced business), and had issued a number of such alternatives. These alternative tests similarly apply to the September and December 2020 quarters when re-testing for actual decline in turnover.

Action required: Re-check whether the 50% of 30% decline threshold applies. Determine your entity’s turnover for the September 2020 quarter as soon as possible after 30 September. Compare to September 2019 quarter BAS. Where applicable, apply the Commissioner’s alternative tests.

Higher or lower rate

For each eligible employee, you must determine whether the higher or lower payment rate applies. This only needs to be done once. Once this has been determined for an eligible employee, the higher/lower rate will apply for them for either or both of stages 1 and 2 as applicable.

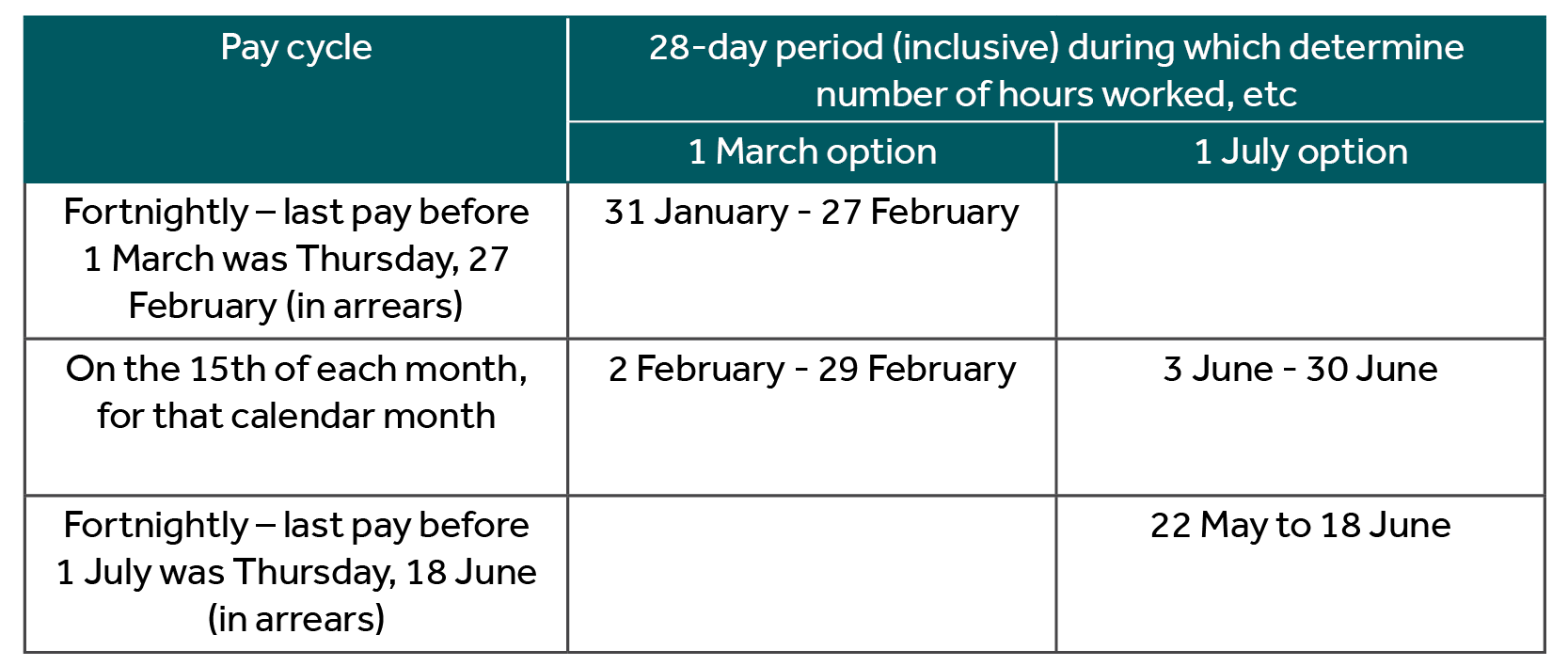

The higher or lower rate is determined based on the number of hours worked in the 28-day period up to the end of the most recent pay cycle ending before either 1 March 2020 or 1 July 2020. This includes time on annual leave, long service leave, sick or personal leave and paid public holidays. You must adopt the high/lower rate for any particular employee based on which 28-day period has the higher number of hours. If the number of hours is 80 or more, the higher rate applies. If under 80, the lower rate applies.

For example:

The purpose of using your pay cycle is to align with your payroll and rostering systems, to reduce compliance costs. Eligible full-time employees during the applicable 28-day period will generally qualify for the higher rate. It is more so eligible part-time and long-term casual employees who might work (including leave, paid public holidays) more or less than 80 hours in the relevant 28-day period.

If employees are paid on a pay cycle that is greater than 28 days, pro-rate the hours to 28 days (eg, worked 90 hours in a 30-day pay cycle ending 27 February. 28/30 x 90 = 84 hours.)

For Eligible Business Participants (EBP), it is fixed as the calendar month of February (despite having 29 days this year) for determining the number of hours. As they are not employees, there are no payroll records. Rather, they must “reasonably demonstrate” the number of hours “actively engaged” in the relevant business in the month of February.

Action required: Analyse payroll records for eligible employees for the applicable pay cycles per above. Pretty much required only for part-time and long-term casual eligible employees. If the number of hours worked (plus on leave, etc) in either applicable 28-day period is 80 or more, allocate that employee to the higher-rate camp. If the number of hours in both applicable 28-day periods was less than 80, allocate that employee to the lower-rate camp. EBPs, document your time “actively engaged” during February in some manner (diary/calendar entries, work output, etc).

Notifications

As noted above, there is no requirement to re-enrol if you are already in the JobKeeper program. However, after dividing your eligible employees into the higher-rate and lower-rate camps, you must make two notifications covering every eligible employee.

Firstly, you must notify the ATO which camp each eligible employee falls into. We expect the form for this will issued shortly, and perhaps can be done through Single Touch Payroll reporting. You will not be eligible to receive next-phase JobKeeper unless this notification is done.

Secondly, within seven days of notifying the ATO, you must notify each eligible employee which camp (higher rate, lower rate) they fall into. There is no standard form for this.

EBPs operating through an entity whose number of active engagement hours in February 2020 was 80 or more must give notice to that effect (no particular form) to the entity in order to receive the higher rate. The entity must notify the ATO (approved form pending) that an EBP is subject to the higher or lower rate, and then must notify the EBP in writing of the rate notified to the ATO. If EBP’s February hours was less than 80 – or they simply don’t provide the notice to the entity where 80 or more – the lower rate will apply.

EBPs operating in their personal name as a sole trader whose number of active engagement hours in February 2020 was 80 or more must state that in a notice to the ATO (approved form pending) in order to receive the higher rate.

Action required: Employers submit the ATO notification as soon as possible, then notify your eligible employees within seven days. The sooner the better, to allow time to resolve any dispute an employee might have over which camp they properly fall into. EPBs attend to their notices.

Minimum wage

The higher/lower rates replace the standard $1,500 per fortnight when the new JobKeeper phase commences on 28 September. The applicable rate (pre-tax) per individual eligible employee must be paid as a minimum in each fortnight.

Action required: Ensure the correct minimum (pre-tax) – higher rate, or lower rate – as applicable is paid to each eligible employee per fortnight from 28 September.

How can Nexia Edwards Marshall NT help you?

Talk to your trusted Nexia Edwards Marshall NT Advisor for any assistance on the next JobKeeper phase.