Welcome to the newest edition of our Not-for-Profit Newsletter. Please feel free to contact us if you have any questions about the content of this Newsletter.

In this edition

This edition covers a number of financial reporting matters including commentary on the lodgement of incomplete financial reports, proposed changes to reporting thresholds, and ACNC best-practice disclosures.

There are also a number of items relating to fraud and compliance, as well as guidance on whistleblowing laws. Finally, we provide details of an NSW Government Initiative that provides a rebate of $1,500 for fees and charges paid by eligible small business, including not-for-profits.

Contents:

- Aged Care

- Financial Reporting Insights

- Fraud

- ACNC Activities

- Ethics

- Compliance

- Public Benevolent Institutions

Elderly to come first

The final report of the royal commission into aged-care quality Care, Dignity and Respect has called for fundamental reform of the aged-care system.

A new act to enshrine the elderlies’ rights should replace its present counterpart by mid-2023, the report recommends. A new Aged Care Commission should be established by the same date.

The recommendations are among 148 that range widely over the sector. The report is in five volumes:

- Volume 1: Summary and recommendations

- Volume 2: The current system

- Volume 3: The new system

- Volume 4: Hearing overviews and case studies

- Volume 5: Appendices

Among recommendations are:

- A new aged-care act that puts older people first, enshrining their rights and providing a universal entitlement for high-quality and safe care based on assessed need. The Aged Care Act (1997) should be replaced with a new act to come into force by no later than 1 July 2023.

- By 1 July 2023, the Australian Aged Care Commission should be established. Its functions would include financial-risk monitoring and prudential regulation of providers.

- The establishment of an Aged Care Pricing Authority to determine prices for specified aged-care services.

- The Aged Care Quality and Safety Commission should be abolished by 1 July 2022, to be replaced by an independent Aged Care Safety and Quality Authority. It would approve and accredit providers, monitor and assess compliance with the quality and safety obligations required of providers under the new act, address non-compliance with them through enforcement, publish information on the outcomes of regulatory actions, including information on system-wide regulatory activity and outcomes, and publish enforcement actions taken against individual providers.

- An inspector-general of aged care would identify and investigate systemic issues and publish reports on findings.

- Plan to deliver, measure and report on high-quality aged care, including independent standard-setting, a general duty on aged-care providers to ensure quality and safe care, and a comprehensive approach to quality measurement, reporting and star ratings.

- Provide up-to-date and readily accessible information about care options and services, and set up a system of ‘care finders’ to support older people in navigating the aged-care system.

- Professionalising the aged-care workforce through changes to education, training, wages, labour conditions and career progression.

- Registration of personal-care workers.

- A minimum quality and safety standard for staff in residential aged care, including an appropriate skills mix and daily minimum staff time for registered and enrolled nurses and personal-care workers for each resident, and at least one registered nurse on site always.

- A simpler and fairer approach to personal contributions and means-testing, including removal of co-contributions towards care, reducing the high effective marginal tax rates that apply to many people receiving residential aged care, and phasing out refundable accommodation deposits.

- Financing arrangements drawing on a new aged-care levy to deliver appropriate funding on a sustainable basis.

- Strengthened provider-governance arrangements to ensure independence, accountability and transparency.

- Governance standards for aged-care providers developed by the Australian Commission on Safety and Quality in Health and Aged Care should require every approved provider, among other things, to have effective risk-management practices covering ‘care’ risks as well as financial and other enterprise risks and consider ensuring continuity of care in the event of default by contractors or subcontractors. A nominated member of the governing body should attest annually on behalf of the members of the governing body that he or she is satisfied that the provider has in place the structures, systems and processes to deliver safe and high-quality care.

- The new act should contain comprehensive whistleblower protections for those receiving aged care, their family, carers, independent advocates and significant others, employees, officers, contractors, and members of the governing body of an approved provider who makes a complaint or reports a suspected breach of quality standards or another requirement of or under the act.

- The Australian government should establish an ongoing program, commencing in the 2021–22 financial year, to help approved providers to improve their governance arrangements, including for ‘care’ governance.

The commissioners recommended monitoring and reporting to support effective and transparent implementation of their recommendations.

They recommended that the federal government respond to them by 31 May.

Prudential-regulation and financial-oversight recommendations

Let’s take a closer look at the prudential-regulation and financial-oversight recommendations:

Responsibility for prudential regulation (Recommendation 130)

From 1 July 2023, the System Governor should be given by statute the role of the Prudential Regulator for aged care with responsibility for ensuring that, under all reasonable circumstances, providers of aged care have the ongoing financial capacity to deliver high-quality care and meet their obligations to repay accommodation lump sums as and when the need arises.

The System Governor should also be given by statute the role of developing and implementing an effective financial-reporting framework for the aged-care sector that complements the purposes of the prudential standards.

Establishment of prudential standards (Recommendation 131)

From 1 July 2023, the Prudential Regulator should be empowered under statute to make and enforce standards relating to prudential matters that must be complied with by approved providers, relating to:

- The conduct of the affairs of providers in such a way as to ensure that they remain in a sound financial position, and ensure continuity of care in the aged-care system, or

- The conduct of the affairs of approved providers with integrity, prudence and professional skill.

Liquidity and capital adequacy requirements (Recommendation 132)

From 1 July 2023, the Prudential Regulator should be empowered under statute to impose liquidity and capital-adequacy requirements on approved providers for the purpose of identifying and managing risks relating to whether:

- Providers have the financial viability to deliver ongoing high-quality care

- Providers of residential care services that hold refundable accommodation deposits can repay them promptly as and when required.

More stringent financial-reporting requirements (Recommendation 133)

From 1 July 2023, the Prudential Regulator should be empowered under statute to require approved providers to submit financial reports.

The frequency and form of the reports should be prescribed by the Prudential Regulator.

Strengthened monitoring powers for the Prudential Regulator (Recommendation 134)

From 1 July 2023, the Prudential Regulator should have the following additional statutory functions and powers, to be exercised in connection with, or for the purposes of, its prudential regulation and financial-oversight functions:

- The power to conduct inquiries into issues connected with prudential regulation and financial oversight in aged care

- The power to authorise in writing an officer to enter and remain on any premises of an approved provider at all reasonable times without warrant or consent, and

- Full and free access to documents, goods or other property of an approved provider, and powers to inspect, examine, make copies of or take extracts from any documents.

Continuous disclosure requirements in relation to prudential reporting (Recommendation 135)

From 1 July 2023, every approved provider should be required under statute to comply with continuous-disclosure requirements to inform the Prudential Regulator of material information of which the provider becomes aware that affects:

- The provider’s ability to pay its debts as and when they become due and payable, or

- The ability of the provider or any contractor providing services on its behalf to continue to provide aged care that is safe and of high quality to individuals to whom it is currently contracted or otherwise engaged to provide aged care.

- The Prudential Regulator should also have the power under statute to designate events, facts or circumstances that may give rise to continuous-disclosure obligations.

Tools for enforcing the prudential standards and guidelines and financial-reporting obligations of providers (Recommendation 136)

From 1 July 2023, the Prudential Regulator should have the powers to take such action, and impose such obligations upon approved providers, as it considers necessary to deal with any breach of the new prudential standards or the financial-reporting requirements, including a failure to comply with continuous-disclosure requirements.

The powers which the Prudential Regulator should be given should include:

- The power to give directions to a provider that mirror those that can be made by the Australian Prudential Regulation Authority pursuant to the Private Health Insurance (Prudential Supervision) Act 2015

- The power to impose administrative penalties in respect of any breach

- The power to apply to a court of competent jurisdiction for a civil penalty in respect of any relevant alleged contravention

- The ability to accept enforceable undertakings, and

- The ability to impose sanctions to limit the ability of the provider to expand its services, revoke accreditation for a service, or revoke approved provider status.

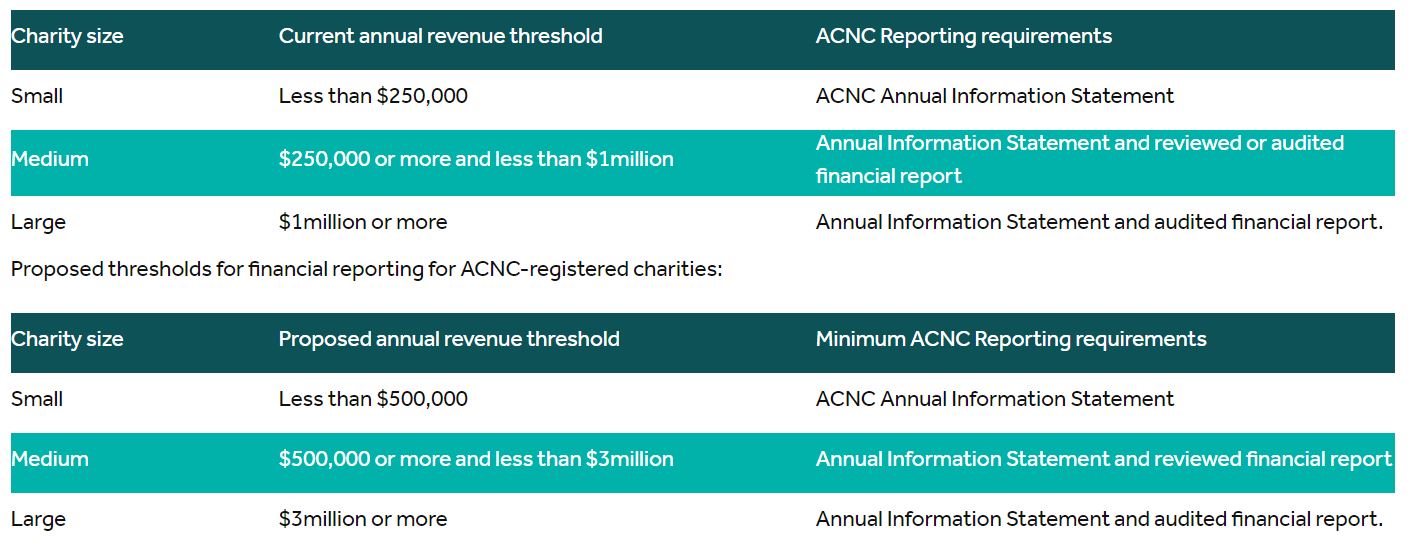

Increasing financial-reporting thresholds for ACNC-registered charities

The Council on Federal Financial Relations has asked that a framework for increasing harmonised financial-reporting thresholds for charities registered with the Australian Charities and Not-for-profits Commission be announced by 30 June.

A consultation paper Increasing financial reporting thresholds for ACNC-registered charities provides a snapshot of present regulatory arrangements, outlines the proposed new reporting thresholds, and sets out key issues for consideration during consultations.

The proposal arises from an independent review of the ACNC, Strengthening for Purpose: Australian Charities and Not-for-profits Commission Legislative Review 2018, which recommended increasing financial-reporting thresholds for ACNC-registered charities.

The recommendation read: ‘Registered entities be required to report based on size with thresholds of less than $1 million for a small entity, from $1 million to less than $5 million for a medium entity and $5 million or more for a large entity’.

Current thresholds for financial reporting for ACNC-registered charities are:

The proposed thresholds are lower than those recommended by an ACNC review panel.

In proposing the thresholds, commonwealth and state governments seek to balance a reduction in regulatory red tape while maintaining transparency to promote accountability, public trust, and confidence in the sector.

A claimed benefit for charities of the reform is that it will decrease professional-service expenses for almost 6800 charities that will move to a lower threshold (representing more than 10 per cent of the sector).

About 3300 charities would move from the medium to small category and no longer be required to produce reviewed financial reports. It would save the charities around $2400 in professional costs annually.

Nearly 3500 charities would move from the large to the medium category and no longer be required to produce audited financial reports. These charities would annually save around $3000 in professional costs.

While the Federal Government can increase ACNC reporting thresholds with relative ease (through changes to regulations), most jurisdictions will need to change legislation or regulations for incorporated associations to ensure that harmonisation continues or to ensure that reporting thresholds for ACNC-registered incorporated associations and other incorporated associations in their jurisdictions remain harmonised.

ACNC-registered charities that are incorporated associations in South Australia, Tasmania, and the Australian Capital Territory would immediately benefit from increases in ACNC reporting thresholds via changes to Commonwealth regulations. This is because state legislation provides that an ACNC-registered entity is exempt from state reporting requirements (including thresholds) as long as the charity is meeting its ACNC-reporting requirements. Victoria also has an exemption in place via a legislative instrument that would also ensure immediate relief to ACNC-registered associations incorporated in Victoria.

Charities filing incomplete financial reports

The ACNC’s annual review of almost 300 medium and large charities’ financial reports has revealed that almost a third of them were incomplete.

The survey showed that 20 per cent failed to disclose the government revenue they had received, and some 5 per cent of those surveyed had inconsistencies in corresponding information in their annual information statements and financial reports.

While reporting had improved, the commission said, there remained areas of concern.

Around 30 per cent of annual financial reports reviewed were missing one or more necessary components. While many charities disclosed government revenue in their financial reports, they failed to do likewise in information statements.

ACNC commissioner Gary Johns urged charities and their accountants, auditors and reviewers to check carefully the financial information they submitted to ensure it was correct and met requirements.

‘Increasingly, potential supporters, donors and the public are looking at information on the charity register to inform their charitable giving. Having a full record of AISs and accurate annual financial reports is an important way for a charity to present itself.’

Medium-sized and big charities are required to submit annual financial reports with their information statements. The reports should include full sets of financials, notes on the statements, a responsible person’s declaration, and a signed audit or ‘review’ report.

Steps towards minimising fraud

The Institute of Internal Auditors in Australia has released 11 steps towards minimising fraud and corruption risks.

They are:

Step 1 – Implement a fraud-and-corruption-control policy

Step 2 – Have ‘zero tolerance’ for fraud – and mean it

Step 3 – Assign fraud-control responsibilities

Step 4 – Perform regular fraud-risk assessments

Step 5 – Develop a fraud-control plan

Step 6 – Implement fraud awareness

Step 7 – Ensure that there is adequate fraud-detection capability

Step 8 – Ensure that there is adequate fraud-investigative capability

Step 9 – Establish fraud-reporting mechanisms

Step 10 – Schedule annual reporting on fraud, including performance measures, and

Step 11 – Commission periodic independent reviews of an organisation’s culture, fraud control, and investigative capability

Drug-and-alcohol counsellor jailed

The Victorian County Court has sentenced Anthony Dieni to 14 years’ jail with a nine-year non-parole period for misappropriating government funds.

He has been ordered to pay $448,805.76 as part of a pecuniary penalty order.

Mr Dieni misappropriated government funds while employed as a drug-and-alcohol counsellor and coordinator at St Paul’s Prevention Rehabilitation, a Strathmore-based charity.

Sentencing follows an investigation (Operation Murano) by the Independent Broad-based Anti-corruption Commission into allegations that Mr Dieni deliberately misled the court in bail applications and sentencing hearings in exchange for cocaine and other drugs of dependence.

IBAC’s Operation Murano resulted in 20 people being charged with a range of offences, including attempting to pervert the course of justice, trafficking in a drug of dependence, and fraud offences.

Childcare director accused of huge fraud

A Canberra childcare-centre director has been accused of defrauding the centre of as much as $500,000.

Police have charged Weston Creek Children’s Centre director Emma Morton with 23 counts of obtaining property by deception, amounting to $160,000 in stolen funds.

Following a raid of Ms Morton’s home in Campbell, a Canberra suburb, officers said they believed that Ms Morton may have taken more than $480,000 from the charity.

In a statement of facts tendered to the court, police alleged that Ms Morton transferred dozens of payments from the childcare centre’s bank account into her own.

Ms Morton, who has been centre director for more than 20 years, allegedly ‘disguised’ $162,753 worth of payments as operating costs.

Police are investigating the loss of another $310,846.

Several transactions in the police submission described personal purchases allegedly made by Ms Morton, including almost $4000 spent at JB Hi Fi, a $3000 chaise longue, and a stay at Hotel Realm in Barton.

Police also alleged that Ms Morton made several transfers worth a total of $130,000 in March and April of last year into a ‘COVID account’ opened in her name.

They are liaising with federal regulators to ensure that the centre, which is a registered charity, can continue operating.

School principal stole $23,000

The principal of a disadvantaged state school in outer-suburban Melbourne has pocketed almost $23,000 in school funds, spending the money on gambling and an overseas family holiday, an ombudsman’s report has revealed.

Victorian Ombudsman Deborah Glass has exposed the theft in the report Investigation of protected disclosure complaints regarding the former Principal of a Victorian public school.

Ms Glass said the theft highlighted ‘systemic weakness in the financial governance of our schools’, rather than a simple theft by a senior staff member.

According to the investigation, the principal asked his staff several times in 2017 and 2018 to counter-sign cheques for school purposes. He then took the cash.

Employed on an annual salary of more than $143,000, the principal had financial problems, including a heavy gambling habit, and significant personal expenses, including rent on inner-city apartments, private-school fees, and the costs of several investment properties in Queensland.

He had a history of financial problems that he did not disclose when he was appointed, including a period of bankruptcy.

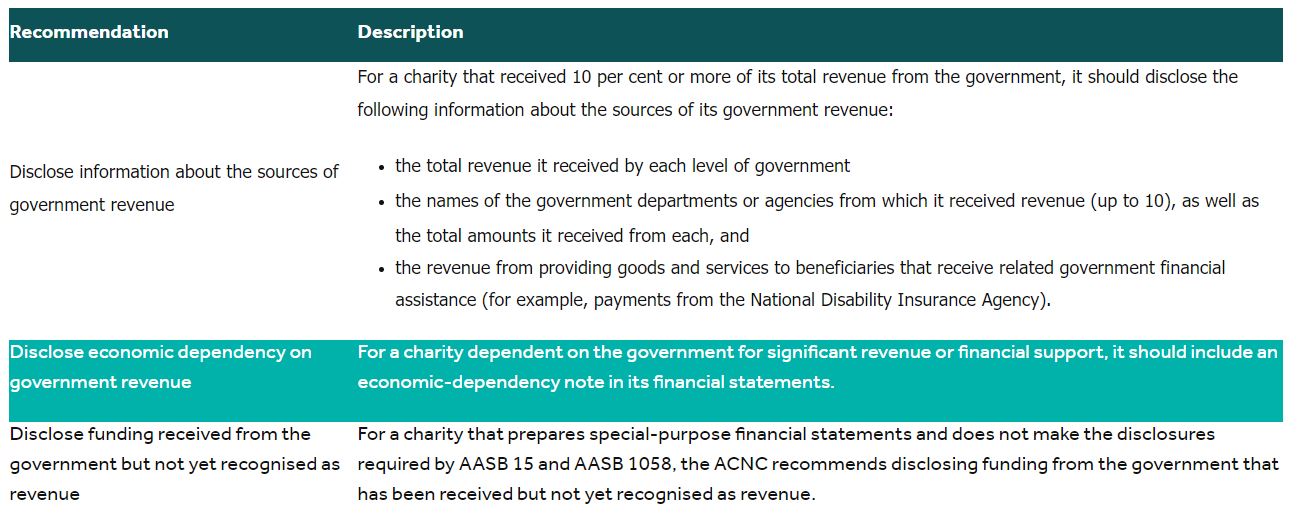

The ACNC has published a new best-practice guide for charities reporting on government revenue they receive.

Donors, funders, supporters, and the public want to know whether a charity receives funds from Government, their size, and who provides them.

Nearly half of charity-sector revenue comes from governments, and increasingly people are viewing financial details on the ACNC’s charity register, often to inform decisions on charitable giving.

Annual Financial Report Disclosures – Best Practice helps charities provide useful, consistent information, enhancing transparency and accountability across the sector.

The ACNC recommends using disclosures to ensure that annual financial-report supplements and matches information in annual information statements.

The commission believes that the move might lead to more cuts to red tape.

Three recommended disclosures of government funding in a charity’s annual financial report are:

For a charity that received 10 per cent or more of its total revenue from the government, it should disclose the following information about the sources of its government revenue:

To ensure that financial statements are clear and easy for users to read and understand, the commission recommends making most disclosures in notes to financial statements rather than in statements themselves.

Recommended disclosures are not intended to replace existing disclosure requirements under Australian accounting standards. For some charities, the recommended disclosures are already required. Rather, they provide the ACNC’s view of best practice in disclosing this kind of financial information and encourage charities to adopt this approach.

Consider the recommendations when preparing your charity’s annual financial report. Take a look at detailed examples and further information in the guide here.

New standard pushes charities towards child-sex redress scheme

A new governance standard aims to incentivise charities to join the national redress scheme for victims of institutional child-sexual abuse.

Governance standard 6 Maintaining and enhancing public trust and confidence in the Australian not-for-profit sector requires a registered charity to take all reasonable steps to join the scheme if a redress claim has been or is likely to be made against it.

The standard came into effect on 25 February via an amendment to the Australian Charities and Not-for-Profits Commission Regulation 2013.

Basic Religious Charities

A Basic Religious Charity is an ACNC category for a particular type of religious charity. Not all charities that are registered with the charity subtype of ‘advancing religion’ are Basic Religious Charities.

Six criteria must be met to be endorsed as a BRC:

- It cannot be entitled to be registered as any other charity subtype (for example, it cannot also be registered with the subtype ‘advancing education’)

- It is not a body corporate registered under the Corporations Act 2001 (including a Registrable Australian Body), an Indigenous corporation registered under the Corporations (Aboriginal and Torres Strait Islander) Act 2006, a corporation registered under the Companies Act 1985 of Norfolk Island, or an incorporated association in any state or territory (including an entity incorporated under Associations Incorporation Act 2005 of Norfolk Island)

- It is not endorsed as a deductible-gift recipient (but it can be endorsed to operate DGR funds, institutions and authorities as long as their total revenue is less than $250,000 for the particular reporting period)

- It has not been approved to report to the ACNC as part of a group

- It has not received more than $100,000 in government grants in the current reporting period and either of the previous two reporting periods, and

- From March 17, it has joined the National Redress Scheme for Institutional Child Sexual Abuse if it has been identified as being involved in the abuse of a person either in an application for redress under the scheme’s section 19 or in response to a request for information from the scheme’s operator (Department of Social Services) under section 24 or 25 of the Redress Act.

A BRC must notify the ACNC of certain changes and submit an annual information statement. It is not required to answer the statement’s financial questions, submit annual financial reports, or comply with governance standards.

The ACNC does not have the power to suspend or remove a member of a BRC’s governing body (what the ACNC calls a ‘a responsible person’).

Related-parties policies are worthwhile

Registered charities must comply with ACNC governance standards to maintain their eligibility for registration (apart from basic religious charities).

Governance standard 5 Duties of Responsible Persons says that a charity must take reasonable steps to ensure that its responsible persons meet certain duties, including:

- To act honestly and fairly in the best interests of the charity and for its charitable purposes • Not to misuse their position

- To disclose any actual or perceived conflict of interest, and

- Ensure that the charity’s financial affairs are managed responsibly.

A responsible person governs a charity. Generally, he or she is a board or committee member, or a trustee.

Conflicts of interest (whether actual or perceived) may arise where a related party has an interest that might conflict with the best interests of the charity. Where a responsible person has an actual or perceived interest with a related party, it might be difficult to demonstrate a duty to act in the charity’s best interests.

Related parties are not defined in the ACNC legislation. The term ‘related party’ is defined by the Australian Accounting Standards Board in AASB 124 Related Party Disclosures.

By having a related-party policy or procedure, charities reduce the risk that their decisions might be influenced by others’ interests. A policy might also help to ensure that related-party transactions do not occur without responsible persons’ approval.

Charity-activity bans broadened

Changes to the ACNC’s governance standard 3 will expand banned activities for registered charities.

The amendments say that, in addition to current governance standards, registered charities:

- Must not engage in conduct that may be dealt with as a summary offence relating to real property, personal property or persons under Australian law, and

- Must take reasonable steps to ensure that their resources are not used, nor continued to be used, to promote or support entities engaging in unlawful activities prohibited under the standard.

The changes respond to recommendation 20 of Strengthening for Purpose: Australian Charities and Not-for-profits Commission Legislation Review 2018.

The purpose of standard 3 is to give the public confidence that a registered charity is governed in a way that is sustainable and consistent with its purposes, and that it protects its assets, reputation, and the people it works with. The amendments are intended to ensure that the standard is more consistent with disqualification as set out in the Charities Act 2013.

Program details allowed

Charities that operate on a calendar year have until 30 June to submit their 2020 annual information statements. For the first time, you may provide details of up to 10 programs demonstrating what your charity does.

New guidance on whistleblowing

The Accounting Professional & Ethical Standards Board has released new guidance to support accountants dealing with whistleblowing and related confidentiality concerns.

Whistleblower laws in Australia aim to protect the confidentiality of individuals who blow the whistle and ensure that they are not victimised for doing so.

Professional accountants’ roles in business, public-sector entities, and public practice make it likely that they will encounter situations involving whistleblowing, whether as the recipients of information or as the party that discovers actual or suspected breaches of laws and regulations.

The 38-page Whistleblowing & Confidentiality – APESB Technical Staff Publication provides guidance on applying APES 110 Code of Ethics for Professional Accountants (including Independence Standards) and other APESB pronouncements to situations that may lead to whistleblowing.

The publication contains eight hypothetical scenarios covering members in business (includes NFPs) and members in public practice, including auditors. The case studies do not provide, however, a guide to the application of whistleblower-protection legislation.

Members involved in circumstances that may lead to whistleblowing are strongly encouraged to seek legal advice or speak to their respective professional bodies to understand their legal and professional obligations.

The publication is available to download on the APESB website here.

Breakthru back-pays more than $2.7m

Disability services provider Breakthru Ltd is back-paying employees more than $2.7 million and has entered into an enforceable undertaking with the Fair Work Ombudsman.

The registered charity, which operates in NSW, Victoria, and Queensland self-reported underpayments to the workplace regulator in March last year.

During new enterprise-agreement negotiations, Breakthru became aware that it had incorrectly classified several employees under applicable awards and industrial agreements, resulting in underpayment of base rates.

In total, Breakthru is back-paying 649 current and former employees $2.75 million (including interest and superannuation) after underpaying them between 2014 and 2020. Individual back-payments range from less than $1 to more than $34,000.

As of 19 February, the company had back-paid 616 workers, less than $47,000 still owing to 33 former employees who had to be back-paid by 31 March.

Fair Work Ombudsman Sandra Parker said that an enforceable undertaking was appropriate as Breakthru had demonstrated a strong commitment to rectifying underpayments.

‘Under the enforceable undertaking, Breakthru has committed to implementing stringent measures to protect the rights of its workforce. These measures include engaging, at the company’s own cost, audits of its compliance with workplace laws over the next two years’, said Ms Parker.

‘This matter demonstrates how important it is for companies to check that they have classified every employee correctly. Any employer who needs help meeting their workplace obligations should contact the Fair Work Ombudsman for free advice and assistance.’

Breakthru is required to display an online notice detailing its workplace law breaches, apologise to workers, commission workplace relations training for human resources, recruitment, and payroll staff, and provide evidence that it has developed systems for ensuring future compliance.

ASIC adopts ‘no-action’ position

The Australian Securities & Investments Commission has temporarily adopted a ‘no-action’ position on convening and holding virtual meetings.

Modifications to the Corporations Act 2001 to facilitate convening and holding meetings using virtual technology were in place under the Corporations (Coronavirus Economic Response) Determination (No.3) 2020.

The determination, which temporarily removed impediments to the use of virtual technology and permitted the dispatch of notices of meetings by electronic means, ceased to have effect on 21 March.

The government has proposed to extend it in the Treasury Laws Amendment (2021 Measures No. 1) Bill. The House of Representatives passed the bill on 17 March and it is awaiting debate in the Senate.

To provide a degree of certainty during COVID, ASIC’s ‘no-action’ position:

- Supports the holding of meetings using appropriate technology – Facilitates electronic notice of meetings, including supplementary notices, and

- Allows more public companies an additional two months to hold their AGMs.

A position on convening and holding meetings using virtual technology applies to meetings held between 21 March and the earlier of:

- 31 October, and

- The date that any measures are passed by parliament on using virtual technology in meetings of companies or managed-investment schemes.

A position on the two-month deferral of AGMs applies to entities with financial years ending up to 7 April.

AAT upholds ACNC ruling

An Administrative Appeals Tribunal decision has endorsed the ACNC’s approach to determining charities’ eligibility for registration as public benevolent institutions.

Previously, the ACNC declined to register Women’s Life Centre as a PBI. Women’s Life got the decision reviewed by the AAT, which in March confirmed the ACNC’s ruling.

Charities in the PBI subtype receive federal tax concessions and may be endorsed as deductible-gift recipients. This, in turn, means that donations to them are tax-deductible.

ACNC assistant commissioner general counsel Anna Longley welcomed the ruling.

‘While all registered charities help our community in one way or another, it was central to the AAT’s decision that services provided by charities registered as a PBI need to be targeted towards those people in our community experiencing serious poverty, distress or misfortune, and for whom the relief provided by a PBI may be vital,’ said Ms Longley.

‘Women’s Life Centre continues to be registered as a charity under two other subtypes.’

There are more than 58,000 charities on the ACNC register, and about 13,800 of them are PBIs.

A 22-page Commissioner’s Interpretation Statement: Public Benevolent Institutions (CIS 2016/03) provides guidance on the meaning and scope of the PBI subtype.