What happened?

Australia essentially has a two-tier tax system – one certain set of tax rules exists for “big” businesses, and another for “smaller” businesses. This second set of rules for smaller businesses means that they are often partial to certain exceptions that big businesses aren’t – such as concessions. Examples include:

- lower corporate tax rates are available for smaller businesses (as compared to their larger counterparts);

- different tax concessions are available for small business entities (SBEs); and

- different small business CGT concessions are available on the sale of small businesses.

While most businesses would love to reap the benefits of these concessions, determining whether your business actually qualifies for them is no easy task. Generally, accessibility to the concessions is determined by ascertaining the business’ amount of aggregated turnover (as explained below) but there’s an added layer of difficulty – the threshold amount changes and differs based on the type of concession from year to year.

How can Nexia Edwards Marshall NT help your business take advantage of these concessions?

The purpose of this alert is to provide you with a brief overview of concessions that may be available for your business. We would be happy to discuss various strategies on how we can assist your business – in particular:

- if you are unsure of whether your current operating structure (i.e. operating as a sole trader, company, trust or partnership) is still appropriate for your circumstances, we can assist you to apply the small business restructure rollover that allows the restructure without tax consequences; or

- if you are thinking of selling your business, we can also assist you in determining whether the small business CGT concessions would apply to your situation to substantially reduce or exempt a capital gain made on the sale.

The Concessions explained – What does this mean for you?

Set out below is a brief overview of the different small business concessions that your business may qualify for.

1. Lower corporate tax rates available for smaller businesses

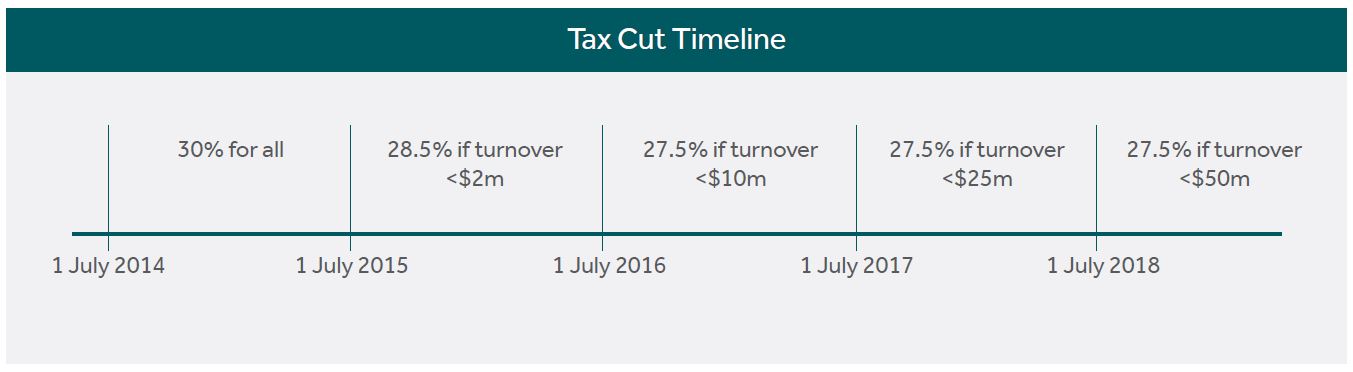

Australia started to gradually lower its corporate tax rate for smaller businesses from 1 July 2015 (i.e. the 2016 income tax year). The Government believes that by lowering the corporate tax rates, Australia will become a more attractive destination for attracting foreign capital (i.e. to compete with the likes of Singapore and Hong Kong that have very low tax rates) and for companies to have more after tax income to invest and employ.

The timeline below illustrates how the corporate tax rates will decrease each year depending on the total aggregated turnover of a company. Pursuant to the current law1, only companies that are carrying on an active business will qualify for the lowered corporate tax rate. That means companies that predominantly invest in cash, shares and property are not eligible for the reduced rates.

Therefore, assuming a company (carrying on a business) has aggregated turnover in the current 2018 income tax year of $20 million, the company will only pay tax at a rate of 27.5% on its 2018 taxable income.

However, with the change in the corporate tax rate to 27.5%, potential franking problems may arise because profits may be taxed at a different rate from the rate at which dividends are franked (i.e. the rate at which shareholders receive franking credits).

For example, this disparity in the different rates can either lead to:

- over-franking (i.e. where a company only pays 27.5% tax on a distribution but shareholders receive a 30% franking credit on receipt of a dividend); or

- trapped franking credits (i.e. where a company pays 30% tax on a distribution but shareholders only receive a 27.5% franking credit on receipt of a dividend).

Speak to your Nexia Edwards Marshall Adviser about possible strategies to avoid over-franking of dividends and therefore, strategies to avoid the obligation to pay franking deficit tax on such over-franked distributions.

Extracting trapped franking credits will be difficult for companies that pay tax on all of their net profit. However, in certain instances, the franking credits may attach to dividends such as where a company has a net trading loss but has cash to pay a franked dividend. Again, your Nexia Edwards Marshall Adviser will be able to assist in appropriate strategies.

2. Different tax concessions available for small business entities (SBEs)

As you may be aware, if you are operating a small business you may qualify for of the following tax concessions:

- Small business restructure rollover (whereby small businesses can transfer assets without any tax consequences between different types of entities including trusts);

- $20,000 immediate asset write-off (e.g. for purchase of depreciating assets that cost less than $20,000);

- Immediate deduction for start-up costs (e.g. for professional legal and accounting advice on how to set up a new business);

- Immediate deduction for certain prepaid expenses (e.g. for prepayment of business insurance);

- Simplified depreciation, trading stock and PAYG rules (e.g. more favourable depreciation rates, no need for end of year stock-take and ATO to calculate PAYG instalments in certain circumstances); and

- Possibility to account for GST on a cash basis and to pay GST by quarterly instalments.

Although the conditions to qualify for each concession are different, the common threshold condition is that small business entities must have an aggregated turnover below a certain amount – currently $10 million.

The timeline below illustrates that from 1 July 2016 the SBE threshold has changed to $10 million (before this time the threshold was $2 million).

These SBE concessions are powerful tools that can financially assist your business. For example, on the sale of a business conducted by a trust for more than 12 months, the capital gain made by the trust will qualify for 50% general CGT discount.

However, if such a business was owned by a company, that CGT discount is not available.

By using the small business restructure rollover relief, such a business operating in a corporate structure may be able to convert its operating structure to a trust and thereby qualify for the CGT discount on the eventual sale of the business.

3. Different small business CGT concessions

Access to the small business CGT concessions – 15-year exemption, 50% active asset reduction, retirement exemption or replacement asset rollover – will remain limited to entities with either (1) a total turnover of less than $2 million [i.e. this test is not increased to $10 million (as for SBEs) or $25 million (i.e. the threshold for the lower corporate tax rate in 2018)] (2) total net asset value (i.e. total assets minus total liabilities) of less than $6 million.

Applying these small business CGT provisions can be very complicated but if applied correctly, these concessions can deliver excellent results on the sale of a business such as:

- No tax on the capital gain on the eventual sale of the business (e.g. provided the business has been carried on for 15 years and the other 15-year exemption conditions have been met);

- Reduced or no tax on the capital gain on the eventual sale of the business (e.g. the concessions can be applied one after the other to reduce the capital gain).

In addition, an amount of $1.415 million (2017 lifetime cap) may be contributed to superannuation if the 15-year exemption or retirement exemption applied to the sale of the business.

No contributions tax (15%) is payable on such contributions and they are not taken into account for the purposes of the concessional and non-concessional contributions caps.

Due to the ever-changing nature and complexity of the tax and superannuation laws, please contact your Nexia adviser so that we can determine whether any of the concessions may apply to your business.

How can Nexia Edwards Marshall NT help you?

Nexia Edwards Marshall NT has a long-standing proven track-record with clients operating all forms of businesses. That experience places us in an excellent position to assist you with practical advice on how to help your business grow and be profitable.

For any questions or to discuss any of the above in relation to your personal situation, please contact Sarah McEachern or your Nexia Edwards Marshall NT Adviser.