You may no longer qualify for the same tax deductions that you claimed last year.

What happened?

Legislation1 was recently enacted whereby, from 1 July 2017 (i.e. the current year), residential property investors may no longer be able to claim either travel deductions incurred in inspecting their residential rental properties, or depreciation deductions on previously used plant and equipment (e.g. ceiling fans, ovens, fridges, carpets, curtains, washing machines, water heaters etc.) used in such residential rental properties.

The law has changed mainly to prevent taxpayers from claiming excessive:

- travel deductions when inspecting their residential rental properties (e.g. prior to 1 July 2017, many taxpayers embarked on so-called “holiday and inspect” trips where individuals would claim for travel costs although the main purpose of the travel was to have a holiday – e.g. inspect a residential investment property for half a day and have a holiday for 14 days and claim travel deductions in full); and

- depreciation deductions on plant and equipment in such residential rental properties (e.g. there was a risk that plant and equipment that has been extensively used by a previous owner or plant and equipment previously used in a taxpayer’s residence for private purposes would either be valued at too high an amount or the same item would be depreciated more than once – leading to excessive depreciation claims).

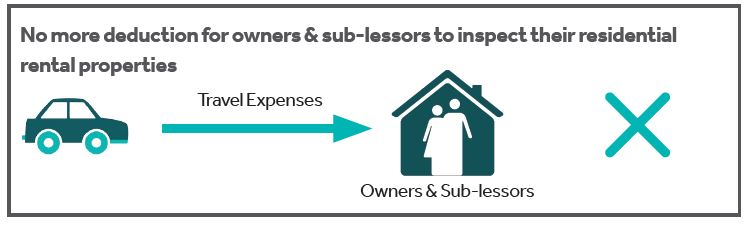

Denial of travel deductions to inspect residential investment properties

From 1 July 2017, individuals, discretionary trusts and SMSFs will no longer be able to claim travel expenses (e.g. motor vehicle expenses, taxi or car hire costs, airfares or public transport costs or meals or accommodation related to the aforementioned travel) incurred to inspect residential rental properties. Such disallowed travel deductions will also not be included in the cost base or reduced cost base of the rental property when calculating capital gains upon the property’s disposal.

However, taxpayers may still claim travel expenses to inspect commercial premises and residential premises used to carry on a business (e.g. a taxpayer carries on a business of property investing, a business of providing retirement living, aged care or student accommodation or property management). Property management expenses paid to real estate agents (which may involve real estate agents incurring travel expenses to inspect the residential rental property) will still be deductible.

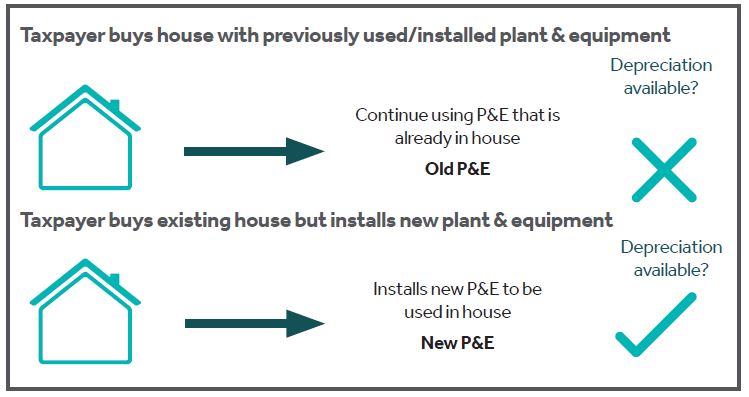

Denial of depreciation deductions on previously used plant and equipment in residential rental properties

From 1 July 2017, allowable depreciation deductions for individuals, discretionary trusts and SMSFs will depend on the time when the items of plant and equipment were acquired (or contracts entered into to acquire such assets). In broad terms:

- for both new and previously used plant and equipment acquired before 9 May 2017, used in a residence that has been a rental property on or before 30 June 2017, owners will still be able to claim a depreciation deduction (irrespective of whether a previous owner had claimed depreciation deductions on the items),

- for new plant and equipment acquired after 9 May 2017, owners will still be able to claim a depreciation deduction over the effective life of the asset. However, taxpayers acquiring previously used items of plant and equipment after 9 May 2017 (e.g. subsequent purchasers of a property containing plant and equipment that was used by the previous owners) will be unable to claim deductions.

Plant and equipment acquired after 9 May 2017 will be “previously used” – and therefore no depreciation deduction would be available if:

- the taxpayer did not use/install the items of plant and equipment originally;

- the items of plant and equipment were used/installed in the residence of the taxpayer or used/installed for a non-taxable purpose (e.g. in a holiday house for private purposes) before the current taxable use.

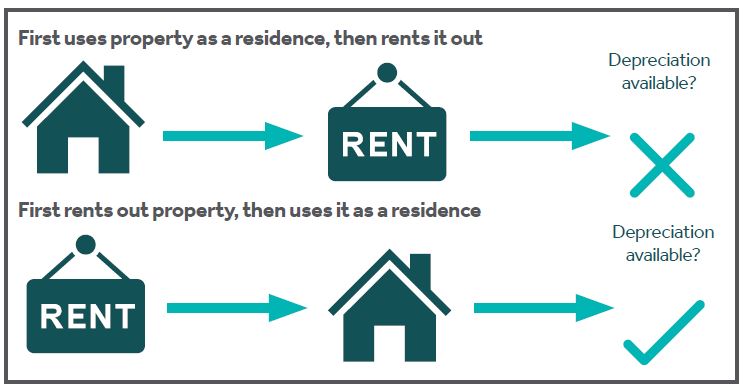

Taxpayers would only be able to deduct depreciation on newly acquired plant and equipment used in residential premises.

Likewise, a taxpayer can only claim depreciation if the plant and equipment was not used in the taxpayer’s residence2 before.

There are some exceptions to the previously used plant and equipment rule when purchasing new residential premises. Generally, a taxpayer can claim depreciation deductions on plant and equipment installed by the developer of the new residential premises because the plant and equipment is trading stock in the hands of the developer (and no depreciation deductions were ever claimed by the developer for such “off-the-plan” purchases.

Where “off-the-plan” sales are not possible, taxpayers buying new premises within 6 months of the premises becoming new residential premises, should qualify for depreciation deductions (i.e. relevant for situations where the developer is unable to find a purchaser for a new apartment and has to rent the apartment until a purchaser is found – provided the lease is less than 6 months, the subsequent purchaser should be able to claim depreciation on the plant and equipment.)

How can Nexia Edwards Marshall NT help you take advantage of these residential rental property changes?

The purpose of the Alert is to provide you with a brief overview of how recent tax changes may affect residential property investors. Due to the ever-changing nature and complexity of the tax laws, please contact Sarah McEachern or your Nexia Edwards Marshall NT adviser so that we can determine how these changes may affect your specific situation.

Nexia Edwards Marshall NT has a long-standing proven track-record with clients in the property market. That experience places us in an excellent position to assist you with practical and tax efficient advice on how to improve your financial position.