Employee or contractor?

It’s an age-old issue for which getting it wrong has generated more and more consequences over time. An oversight such as treating someone as an independent contractor when in fact they are an employee could lead to a number of unwanted consequences.

What consequences might arise from making that error?

- Failure-to-PAYG-withhold penalty

- Superannuation Guarantee shortfall, penalties and interest

- Denial of deductions

- Fringe Benefits Tax, penalties and interest

- Invalid claim for GST credits, plus penalties and interest

- Payroll tax liability, penalties and interest

- Employee entitlements liability (annual leave, long service leave, allowances, etc)

- Underinsurance for workers’ compensation

- Exposure to vicarious liability for employee’s acts

And possibly more. Getting this wrong can be very costly indeed – business-destroying if on a large enough scale. The latest development on this issue is two recent High Court decisions. These have disrupted the established way of going about determining whether a person is an employee or independent contractor. Business owners need to take note, and possibly act to mitigate any uncertainty over employee/contractor relationships.

High Court resets goalposts

The two recent cases are CFMMEU v Personnel Contracting [2022] and ZG Operations v Jamsek [2022]. The disputes were over obligations under the Fair Work Act 2009, but the implications go far beyond that as you can see in the non-exhaustive list above.

In the CFMMEU case, a labourer was engaged by Personnel Contracting, a labour-hire company. The contract between them stated that the labourer was a self-employed contractor, but was to attend the site of Personnel Contracting’s client at nominated times, and provide his labour as required. He also provided his own clothing and boots, but was supplied with all other equipment, and worked a regular pattern. The labourer issued his invoices for payment.

In ZG Operations, two truck drivers worked for the company for many decades. They were employees until the mid-1980s, after which they set up partnerships with their wives, executed contracts for the provision of transport services, and supplied their own trucks. They were required to be at the company’s disposal for nine hours a day, five days a week. The partnerships issued invoices for payment.

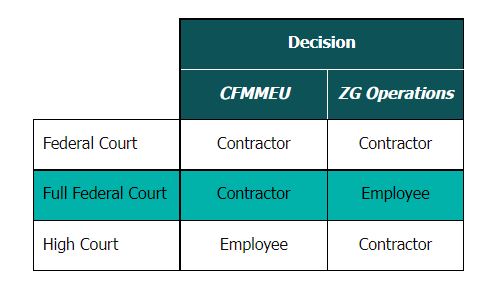

In both cases, the paying parties treated the individuals as independent contractors. But here is the roller-coaster pathway of decisions through the courts:

The Federal Courts applied the precedent “multi-factorial” approach, which considers the “totality of the relationship” between the parties. This includes the manner of conduct and behaviour between the parties in addition to the contractual relationship. It’s essentially a substance-over-form approach that has been the established way of addressing the “employee v contractor” question for decades. However, the High Court has now decided that that is not the appropriate way to decide the matter where the following three conditions are satisfied:

- Written contract with clear, comprehensive terms

- The contract is not a sham

- The contract does not breach any laws such that it is rendered invalid

If they are all satisfied, the contract terms are paramount, and are what decide the matter. In other words, the substance of the relationship is to be found in the contract terms, and the manner of conduct and behaviour amongst the parties does not interfere with that. For example, if a contract gives the supplier the right to delegate (indicative of being a contractor), it does not matter if the supplier in practice never actually does so. What matters is that they have the right to delegate. The High Court determined in both cases that all three conditions were satisfied, and thus the terms of the respective written agreements were the determinative factor.

Although it was not expressly said so, if any one of the above conditions is not satisfied, presumably we revert back to the multi-factorial approach. On that basis, assuming the second and third conditions above are satisfied, what determines where the substance of a relationship (ie, employee or contractor) is to be found – multi-factorial approach or contract terms – is whether there is a written contract with clear, comprehensive terms.

Review contractor agreements

It would be prudent to review existing agreements with contractors to ensure they are comprehensive and clear, and appropriately reflect a contractor relationship. Otherwise, there is a risk that they are found to be employees, and, well, refer to that above list of consequences.

PAYG withholding, superannuation guarantee

The rules for PAYG withholding set out a number of payment categories from which the payer must withhold. This includes payments to an “employee”. These cases decided disputes over who is an employee under the Fair Work Act 2009, not tax legislation. However, both sets of laws draw upon the ordinary meaning of the word “employee” – which is what these cases addressed. Accordingly, it would seem fair to say that the decisions would be applicable in determining whether a person is an employee for PAYG withholding purposes.

The rules setting out Superannuation Guarantee (SG) obligations are a little different. They impose the obligation in relation to employees in the ordinary sense, and thus again it would seem fair to say that these decisions are applicable in determining who is an employee for SG purposes. However, the SG rules go further, and impose SG obligations beyond employees, including in relation to persons working under a contract that is wholly or principally for their labour (ie, more than half of the value of the contract). Accordingly, it is possible for a person to not be an employee for PAYG withholding purposes, but they are for SG purposes. That is, no withholding required, but must pay SG.

ATO guidance

The ATO has a number of guidance pronouncements relating to employer obligations, such as PAYG withholding (TR 2005/16) and SG (SGR 2005/1). The ATO has commented that these pronouncements are under review in light of these decisions.

Contracting through a company

Where a person provides their services through their own company (as opposed to in their personal name), the impact of these decisions would be limited. The reason is that the contractual relationship is with the company, not the individual. However, there are a number of integrity laws at both federal and state level to combat inappropriate tax outcomes under these arrangements.

Talk to Sarah McEachern or your trusted Nexia Edwards Marshall NT advisor about ensuring your arrangements with contractors are clear, and that you are appropriately managing your risks and obligations as an employer.