With 2017 drawing to a close, employers should be aware of the tax consequences of hosting Christmas parties for their staff.

Employers must pay fringe benefits tax (FBT) – at a rate of 47%1 on the grossed-up taxable value – when certain non-cash benefits (called fringe benefits) are supplied to their employees or their associates (i.e. past, future and current employees and their spouses and children) instead of paying salary or wages.

However, sometimes these non-cash benefits will not be subject to FBT. While the FBT law does not specifically deal with Christmas parties, the following types of FBT exempt benefits are particularly relevant when determining an employer’s FBT liability when hosting a Christmas party:

- Exempt minor and infrequent benefit valued at less than $3002 (e.g. a catch-all exemption available for current employees and their associates for low value benefits provided on an “infrequent” or “irregular” basis);

- Exempt property benefit3 (e.g. all Christmas party food and drink provided by the employer that is consumed by a current employee at a party, provided the party was held at the employer’s premises on a business day); and

- Exempt transport benefits4 (e.g. a current employee’s employer pays for a taxi ride home if the Christmas party is held at the employer’s premises).

Please note that the $300 minor and infrequent benefit exemption applies separately on a per benefit basis (i.e. minor benefit exemption can apply if one present of $250 is provided to an employee and another present of $290 is provided to the employee’s spouse).

Also, the minor benefits exemption is not available for meal entertainment fringe benefits (e.g. food and drink at the Christmas party) if the employer uses the 50:50 split method when preparing the annual FBT return (i.e. where 50% of the GST-inclusive cost of total meal entertainment is subject to FBT and the other 50% is not) to value meal entertainment. For the minor benefit exemption to apply, the actual method to value meal entertainment expenses must be used.

What is the best way to party (for tax purposes)?

As you can see from the above, the amount of FBT payable can be influenced by:

- When the party will be held (i.e. for the minor and infrequent benefit exemption the cost of the benefit provided must be less than $300 per head and not provided regularly or frequently);

- Where the party will be held (i.e. for the property fringe benefit exemption to apply, the food and drink must be provided and consumed by current employees on the employer’s premises on a business day);

- For whom the party will be held (i.e. the tax consequences are different depending on whether the benefits are provided to employees, their associates or clients).

Interaction of FBT, income tax and GST

As a general rule, when providing taxable fringe benefits to employees or their associates, an employer may be able to claim GST credits and income tax deductions in respect of expenses incurred. However, no GST credits or tax deductions may be claimed when providing FBT exempt benefits to such a group.

More specifically, the income tax and GST treatment will depend on whether the benefit is an entertainment or non-entertainment benefit:

- If the benefit is an entertainment benefit (e.g. a movie ticket or a Christmas meal) – the employer may not claim income tax deductions or GST credits on the cost of providing this benefit;

- If the benefit is not an entertainment benefit (e.g. a Christmas hamper5) – the employer may claim income tax deductions and GST credits on the cost of providing this benefit.

We have mapped out the different tax consequences arising from two different scenarios (i.e. whether the Christmas party is held on the employer’s premises during a work day or not). To highlight the differences between these two scenarios, we have assumed that in both scenarios, only current employees, their spouses and clients attend the event and the employer provides the following benefits to each attendee:

- food and drink at the Christmas party;

- an entertainment gift (e.g. a movie ticket); and

- a non-entertainment gift (e.g. a Christmas hamper).

We have also assumed that such benefits have not been provided on a regular and frequent basis throughout the year.

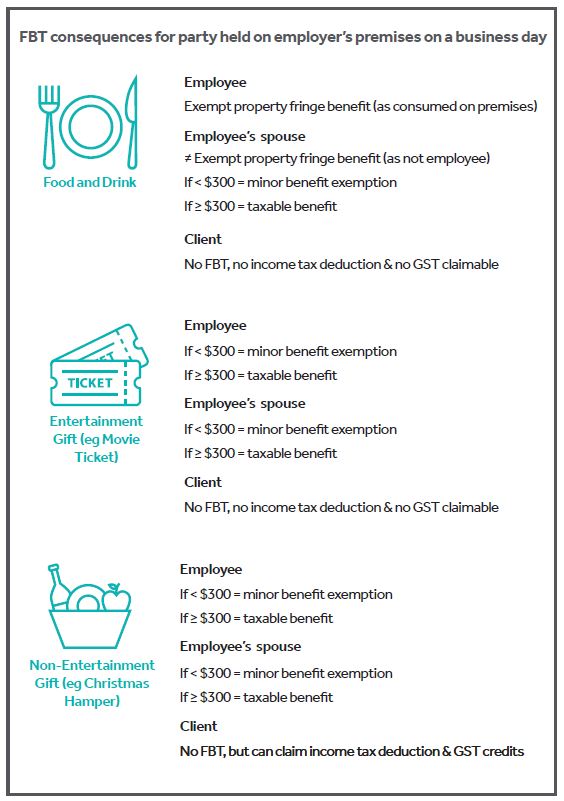

1. Christmas party held on employer’s premises

Although this is more common for informal business celebrations (e.g. Friday night drinks), employers who hold their Christmas party on their business premises on a work day can save on FBT (mainly due to the exemption for food and drink consumed on the premises by current employees).

This is illustrated by the diagram below:

Please note that if the employer pays for the current employee’s taxi trip home after the party, this will also be an exempt transport fringe benefit because the trip is a single trip that begins at work6 and ends at the employee’s home7.

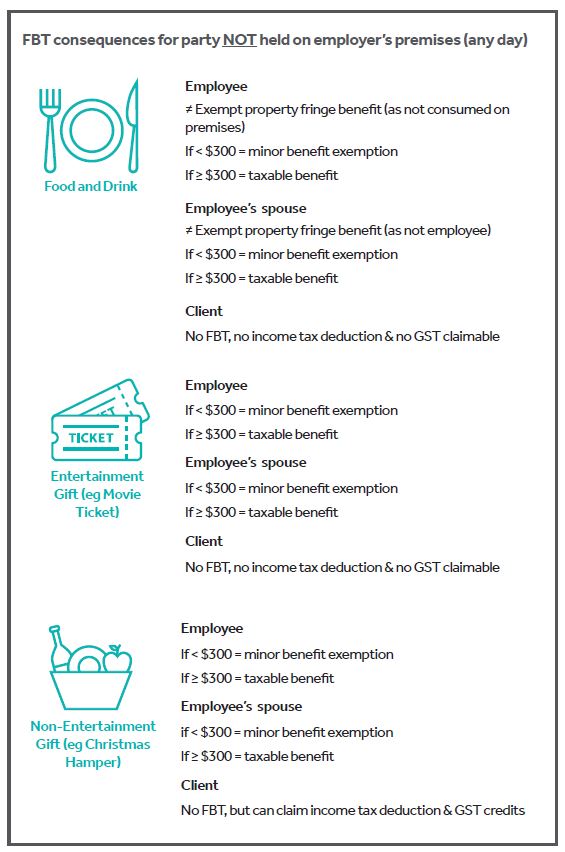

2. Christmas party NOT held on employer’s premises

Regardless of the potential FBT savings, more commonly, employers hold Christmas parties off-site.

The tax consequences of hosting such off-site parties are illustrated in the diagram below:

Please note that if the employer pays for the current employee’s taxi trip home after the party, this will NOT be an exempt transport fringe benefit because the trip is not directly home from the employer’s premises.

However, the benefit may be exempt under the minor benefits exemption provided the taxi fare (as well as any associated benefits – for example if the Christmas party food and drink was provided in conjunction with the taxi fare) – is less than $300.

How can Nexia Edwards Marshall NT help you?

This brief overview gives a broad outline of the application of the FBT law to Christmas time activities. A variety of benefits may be supplied to employees at Christmas time with each containing their own valuation, deduction and exemption rules.

Please contact Sarah McEachern or your Nexia Edwards Marshall NT Adviser if you would like to discuss any of the issues mentioned in more detail.

The Partners, Directors and staff of Nexia Edwards Marshall NT sincerely wish you a restful and happy Christmas and a successful 2018.