JobKeeper was necessarily designed and implemented in a very short time-frame, and so some waste had to be accepted in return for haste. Treasury has now had the opportunity to review the program. The government yesterday announced plans for a second phase of the JobKeeper program for business. However, the eligibility criteria will be tightened, and it will be more precisely targeted.

The current JobKeeper program will continue unchanged until its completion on 27 September.

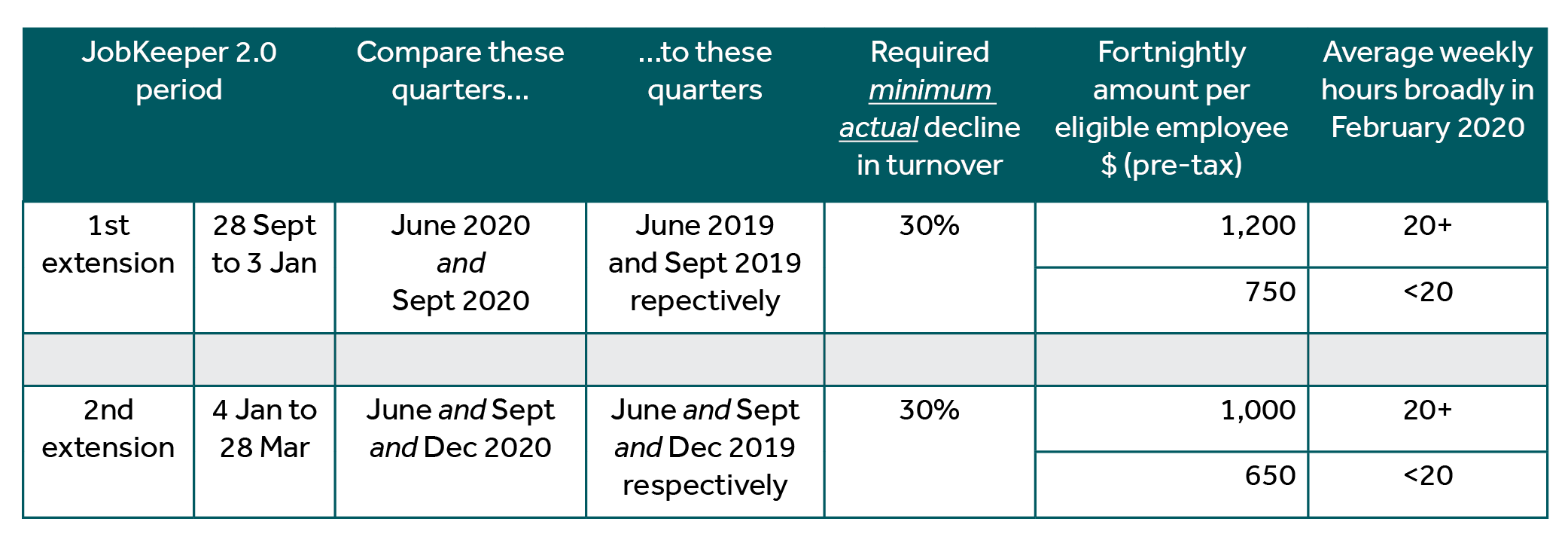

JobKeeper 2.0

The government has decided to extend the JobKeeper program for an additional six-month phase, from 28 September 2020 to 28 March 2021. This comprises 13 fortnights, but will be divided into two periods; the 1st extension period of seven fortnights, and the 2nd extension period of six fortnights. JobKeeper 2.0 is estimated to cost $16.6 billion.

Re-test decline in turnover

Qualifying for JobKeeper 2.0 requires a re-testing of decline in turnover. The decline percentages of 30% for businesses with group-wide turnover of $1 billion or less, 50% for other businesses, and 15% for certain not-for-profits are retained, but the test will be applied differently. It will now look back to actual turnover results. No predictions will be required. For simplicity, we’ll continue by referring to businesses and the 30% threshold.

1st extension period: 28 September 2020 to 3 January 2021

To qualify for the 1st extension of JobKeeper 2.0, a business must compare it’s actual turnover for the June 2020 quarter to that in the June 2019 quarter, and same again with September 2020 and 2019 quarters. The test is passed if there was a decline of at least 30% in both comparisons (ie, quarter-to-quarter, not combined overall). The turnover figures can generally be taken from your Business Activity Statements (BAS). The Commissioner of Taxation will have a discretion to set out alternative tests where there aren’t comparable quarters last year, much like the existing discretion.

The period then has two payments rates – $1,200 and $750. An eligible business will receive the higher or lower payment rate for an eligible employee based on the employee’s weekly average hours of work in the “four weeks of pay periods” before 1 March 2020 (broadly, the month of February 2020). If the employee’s weekly average is 20 hours or more, the higher rate applies. If under 20, the lower rate applies. The ATO will provide guidance where a business’s pay periods do not neatly fit into weekly or fortnightly periods.

You will need to analyse your payroll records from February this year to determine which rate applies to each or your eligible employees. (There are no changes to the conditions for being an eligible employee.) That will also determine the minimum amount that you must pay to each individual eligible employee ($1,200 or $750, as applicable, pre-tax) in each JobKeeper fortnight.

Once you have determined that a particular eligible employee was above or below that 20-hour threshold, the applicable higher or lower rate will apply to that employee for both extension periods.

2nd extension period: 4 January to 28 March 2021

The 2nd extension period operates much the same, but with two key differences. Firstly, you must again re-test decline in turnover, by comparing the June, September and December 2020 quarters to the equivalent quarters in 2019. To qualify, all three comparisons must show a decline of at least 30%. Secondly, the two payments rates fall to $1,000 and $650.

Snapshot

Here’s a summary:

A business might qualify for the 1st extension period, but not the 2nd (because December 2020 quarter turnover did not actually decline by 30% or more). However, if you don’t satisfy the decline in turnover test for the for the 1st extension, that means you won’t satisfy it for the 2nd extension.

Other issues

For an Eligible Business Participant, the higher of lower rate is based on weekly average number of hours “actively engaged” in the business back in February. That presents issues for supporting the number of hours, as there are no payroll records.

The Commissioner will have a discretion to set out alternative tests to measure an employee’s working hours in that February period where they were out of the ordinary (eg, the employee was on leave, commenced employment during that period, etc).

Complementary amendments will be made to the Fair Work Act.

What now?

There will be details to clarify upon the JobKeeper Rules being amended by the Treasurer to reflect JobKeeper 2.0. But for now, to get a preliminary idea of whether your business will qualify for the 1st extension period of JobKeeper 2.0, you’ll need to compile the following information:

- Turnover for the June 2019, September 2019 and June 2020 quarters (refer to your BASs)

- Analyse your payroll records for February 2020 to allocate your current eligible employees into the above/below 20 hours category

- Determine your turnover for the September 2020 quarter as soon as possible after the quarter end.

The first fortnight for JobKeeper 2.0 ends on Sunday, 11 October. Between now and then, with the above information, and a few details ironed out in due course, you will be able to determine the following:

- Whether you qualify for the 1st extension period

- If you do, the allocation of your eligible employees to the higher or lower payment category

- The applicable minimum amount that you must pay to each eligible employee ($1,200 or $750, pre-tax) by 11 October (or such later date as the Commissioner is likely to determine), and then on for the remaining six fortnights in the 1st extension period.

Talk to your trusted Nexia Edwards Marshall NT Advisor about how we can help you determine whether you qualify for the 1st extension period of JobKeeper 2.0, and what you need to do.