The classification of loans subject to covenants are expected to change following amendments to accounting standards.

At a glance

- A liability is classified as non-current where an entity has the right, at balance date, to defer settlement of the liability for at least twelve months after balance date.

- Hence, covenants or conditions that the entity must meet on or before balance date affects the classification of a loan at balance date.

- However, covenants or conditions that the entity must meet after balance date (including a lender’s annual covenant review) do not affect the classification of a loan at balance date.

- New disclosures are required for loans with covenants and conditions classified as non-current liabilities that could become payable within twelve months after balance date.

The AASB issued AASB 2022-6 Amendments to Australian Accounting Standards – Non-current Liabilities with Covenants (‘the 2022 Amendments’) relating to the classification, as either current or non-current liabilities, of bank and other loan arrangements that are subject to covenants and other conditions. The 2022 Amendments alter and build upon other amendments contained in AASB 2020-1 Amendments to Australian Accounting Standards – Classification of Liabilities as Current or Non-current (‘the 2020 Amendments’).

The 2020 Amendments and 2022 Amendments (collectively, ‘the amendments’) are to be applied at the same time. Consequently, this publication considers the combined effects of the amendments.

The revised paragraph 69 of AASB 101 requires an entity to classify a liability as current when:

a) it expects to settle the liability in its normal operating cycle; or

b) it holds the liability primarily for the purpose of trading; or

c) the liability is due to be settled within twelve months after the reporting period; or

d) it does not have the right at the end of the reporting period to defer settlement of the liability for at least twelve months after the reporting period.

Subject to meeting the other criteria in paragraph 69(a)-(c), the amendments clarify that a liability is classified as non-current when the entity has the right at balance date to defer settlement of the liability for at least twelve months after the reporting period. That right must have substance and must exist at balance date.

The amendments do not affect the classification of on-demand or at-call liabilities, provisions, or other liabilities where the entity does not have the right to defer settlement for more than twelve months after balance date.

Loans subject to conditions

Many long-term loan arrangements contain conditions and covenant that the entity must comply with, otherwise the lender can require the entity to repay some or all of the outstanding loan.

The amendments introduce new provisions to determine when a long-term loan liability that is subject to the entity complying with conditions and covenants is classified as current or non-current.

Although the amendments refer to these conditions as ‘covenants’, loan conditions may be broader than just financial ratio covenants such as times interest cover or working capital and loan to value (LVR) ratios. Loan conditions may include covenants such as an entity not incurring capital expenditure or paying dividends over a specified amount or providing the lender with quarterly management accounts or audited annual financial statements.

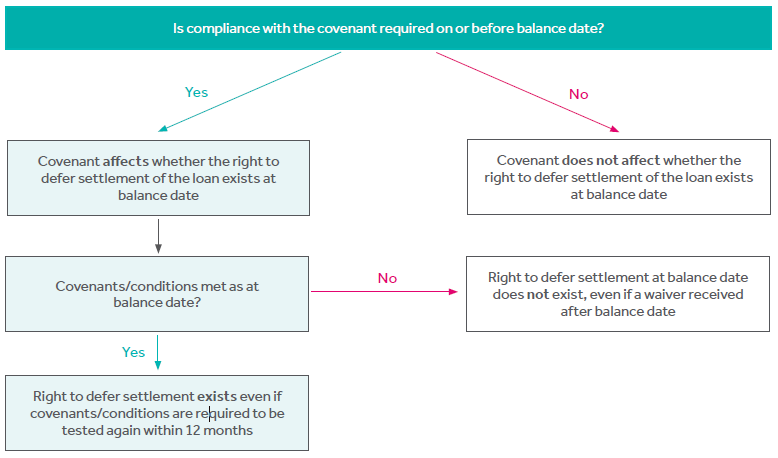

The classification of a liability as current or non-current is based on the entity’s right to defer settlement of a liability for at least twelve months after the reporting period that exists at balance date. In determining whether an entity has that right at balance date, it considers whether it is required to comply with the covenant or condition on or before balance date or only after balance date.

Compliance with a covenant at balance date affects whether the right exists at that date even if compliance with that covenant is assessed or determined only after the reporting period.

However, if the entity is required to comply with the covenant only after balance date the existence of that covenant does not affect whether the entity has the right to defer settlement at balance date. For example, a covenant based on the entity’s working capital position six months after balance date does not affect the classification of the liability at balance date.

The new requirements can be illustrated as follows:

Effect of events after balance date

In classifying a liability as either current or non-current, the amendments reinforce the primacy of the entity’s right at balance date to defer settlement of a liability for at least twelve months after the reporting period. Where the entity has such right at balance date, the liability is classified as non-current regardless of events that occur after balance date.

Consequently:

i) When an entity breaches a covenant of a long‑term loan arrangement on or before balance date with the effect that the liability becomes payable on demand, it classifies the liability as current even if the lender agreed, after balance date and before the authorisation of the financial statements for issue, not to demand payment because of the breach. This is because, at balance date, the entity does not have the right to defer settlement of the liability for at least twelve months after that date.

However, if the lender agreed on or before balance date to provide a period of grace ending at least twelve months after the reporting period, during which the lender cannot demand immediate repayment, then the entity classifies the liability as non‑current.

ii) If a liability meets the criteria in paragraph 69 of AASB 101 for classification as non-current, it is classified as non-current even if management intends or expects to settle the liability within twelve months, or even if the entity settles the liability between the end of the reporting period and the date the financial statements are authorised for issue.

iii) If an entity has the right at balance date to defer settlement of a liability for at least twelve months after balance date, the liability is classified as non-current even if the entity breaches a condition after balance date but before the financial statements are authorised for issue. This is because at balance date the entity had the right to defer settlement of the liability, notwithstanding the occurrence of the subsequent event.

The above events represent new events or conditions occurring after balance date which do not alter the entity’s rights that existed at balance date. Consequently, they would be disclosed as non‑adjusting subsequent events in accordance with AASB 110 Events after the Reporting Period.

Additional disclosures

As a result of the amendments an entity might classify a loan as non-current when its right to defer settlement of the liability is subject to it complying with covenants after balance date.

In such situations, new paragraph 76ZA of AASB 101 requires the entity to disclose information about non-current loan liabilities that could become repayable within twelve months after the reporting period, including:

a) information about the covenants (including the nature of the covenants and when the entity is required to comply with them) and the carrying amount of related liabilities; and

b) facts and circumstances, if any, that indicate the entity may have difficulty complying with the covenants. Such facts and circumstances could also include the fact that the entity would not have complied with the covenants if they were to be assessed for compliance based on the entity’s circumstances at the end of the reporting period.

Settlement of a liability

The amendments also clarify that settlement of a liability occurs where there is an outflow of resources from the entity – which could be by way of transfer of cash or other assets or services, or by the transfer of the entity’s own equity instrument – that results in the extinguishment of the liability. Hence, a liability that is rolled over under an existing loan facility does not constitute settlement because it is the extension of an existing liability and does not involve any transfer of economic resources.

A bond that is classified as a liability that the holder may convert to equity before maturity is classified as current or non-current according to the terms of the bond. However, the terms of a bond that contains a conversion option that meets the definition of an equity instrument by AASB 132 (ie, fixed for fixed criteria) and is recognised separately from the host liability does not affect its classification as current or non-current.

Examples

The following examples illustrate the new requirements.

Example 1: Covenant tested annually based on audited financial statements

Company A has a long-term bank loan repayable after 5 years. The loan requires Company A to have a working capital ratio above 2.0 as at every 30 June, failing which the lender has the right to require repayment of the loan. The covenant is assessed based on Company A’s audited annual financial statements which are required to be provided to the bank by 31 October. Company A’s balance date is 30 June.

On 30 June 20X2, Company A’s working capital ratio is 1.85. Company A’s working capital ratio has improved to 2.5 by 31 October 20X2.

How does Company A classify the loan on 30 June 20X2?

Assessment

AASB 101.72B(a) states that a covenant affects whether the right to defer settlement for at least twelve months after balance date exists if an entity is required to comply with the covenant on or before the end of the reporting period. This is the case even if compliance with the covenant is assessed only after the reporting period.

Company A is required to comply with the covenant on 30 June 20X2 even though its compliance is only assessed after balance date by providing its 30 June 20X2 audited financial statements to the bank. Therefore, the covenant affects whether the right to defer settlement exists at 30 June 20X2.

Company A’s working capital ratio on 30 June 20X2 is 1.85, which is below the required ratio of 2.0. Therefore, at 30 June 20X2 Company A does not have the right to defer settlement of the liability for at least twelve months after the reporting period. The bank loan is classified as current at 30 June 20X2, even if Company A receives a waiver from the bank after 30 June 20X2.

Example 2: Covenant to be met after the end of the reporting period

Company A has a bank loan repayable in 5 years. The loan requires Company A to have a working capital ratio above 2.0 at each annual review date which is 15 June, failing which the lender has the right to require repayment of the loan. Company A’s balance date is 31 December.

Company A’s current ratio was:

- 2.5 at 15 June 20X2

- 1.8 at 31 December 20X2

How does Company A classify the loan at 31 December 20X2?

Analysis

Company A had met the covenant at its annual review on 15 June 20X2 and therefore, the loan is not repayable on demand at 31 December 20X2.

AASB 101.72B(b) states that covenants that an entity is required to comply with after the reporting period does not affect whether an entity has the right to defer settlement at the end of the reporting period.

Company A is required to comply with the covenant next on 15 June 20X3, which is after the current reporting period. Therefore, this covenant does not affect the determination of whether Company A’s right to defer settlement exists at 31 December 20X2.

That Company A’s current ratio at 31 December 20X2 is less than 2.0 does not affect its compliance with the covenant as compliance is only tested at the annual review date (15 June 20X3). An expectation that the covenant may not be met at the next annual review date does not affect the classification of the liability at 31 December 20X2. The bank loan is classified as non-current.

As required by AASB 101.76ZA, Company A discloses information that enables users of financial statements to understand the risk that the liability could become repayable within twelve months after the reporting period. This includes information about the covenant (including the nature of the covenant and when the entity is required to comply with them), the carrying amount of related liability (the bank loan), and any facts and circumstances that indicate Company A may have difficulty complying with the covenant.

Example 3: Covenant tested quarterly

Company A has a long-term bank loan repayable after 7 years. The loan requires Company A to have a working capital ratio above 2.0 at each quarter ended 31 March, 30 June, 30 September, and 31 December, failing which the lender has the right to require repayment of the loan. Company A’s balance date is 30 June.

Company A’s working capital ratio at 30 June 20X2 is 3.2 and exceeded 2.0 in each preceding quarter.

How does Company A classify the loan at 30 June 20X2?

Analysis

Company A has met the covenant on 30 June 20X2 (and the preceding quarters) and therefore, the loan is not repayable on demand at 30 June 20X2.

AASB 101.72B(b) states that covenants that an entity is required to comply with after the reporting period does not affect whether an entity has the right to defer settlement at the end of the reporting period.

Company A is required to comply with the covenant next on 30 September 20X2, which is after the current reporting period. Therefore, this covenant does not affect the determination of whether Company A’s right to defer settlement exists at 30 June 20X2. An expectation that the covenant may not be met at a future assessment date does not affect the classification of the liability at 30 June 20X2. The loan is classified as non-current.

As required by AASB 101.76ZA, Company A discloses information that enables users of financial statements to understand the risk that the liability could become repayable within twelve months after the reporting period. This includes information about the covenant (including the nature of the covenant and when the entity is required to comply with them), the carrying amount of related liability, and any facts and circumstances that indicate Company A may have difficulty complying with the covenant

Example 4: Material adverse events clauses

Company A has a long-term bank loan repayable after 7 years. The loan is subject to an annual review which permits the lender to require repayment of the loan if there has been a material adverse change in the company’s financial condition.

The annual review date of the loan facility is 15 April. The lender completed its annual review on 15 April 20X2 and Company A satisfied the conditions of the facility. Company A’s balance date is 30 June.

How does Company A classify the loan on 30 June 20X2?

Analysis

The lender completed its annual review on 15 April 20X2 and Company A satisfied the conditions of the facility. Therefore, the loan is not repayable on demand at 30 June 20X2.

As provided by AASB 101.72B(b), covenants that an entity is required to comply with after the reporting period does not affect whether an entity has the right to defer settlement at the end of the reporting period.

Company A is subject to the next annual review on 15 April 20X3, which is after the current reporting period. Therefore, this covenant does not affect the determination of whether Company A’s right to defer settlement exists at 30 June 20X2. The loan is classified as non-current.

As required by AASB 101.76ZA, Company A discloses information that enables users of financial statements to understand the risk that the liability could become repayable within twelve months after the reporting period. This includes information about the covenant (including the nature of the covenant and when the entity is required to comply with them), the carrying amount of related liability, and any facts and circumstances that indicate Company A may have difficulty complying with the covenant.

Application date and transition

Both the 2020 Amendments and the 2022 Amendments mandatorily apply to annual reporting periods beginning on or after 1 January 2024 and are applied retrospectively. Earlier application is permitted.

An entity early adopting the 2022 Amendments must also adopt the 2020 Amendments at the same date.